Australian Government-Backed Business Loans: Grants, Subsidies and Support Programs

Australian Government-backed business loans, grants, subsidies and support programs are publicly funded schemes designed to help small and medium businesses access capital, reduce costs, and grow. They range from zero-interest loans and repayable advances to outright grants that never need to be paid back. Eligibility varies by industry, location, business size, and what the money is for — and most programs are administered through business.gov.au or equivalent state portals.

Quick answer

Australian Government-backed business loans, grants, subsidies and support programs are publicly funded schemes designed to help small and medium businesses access capital, reduce costs, and grow. They range from zero-interest loans and repayable advances to outright grants that never need to be paid back. Eligibility varies by industry, location, business size, and what the money is for — and most programs are administered through business.gov.au or equivalent state portals.

Key takeaways

- Grants are free money; loans must be repaid. Knowing the difference saves wasted applications.

- The Australian Government's Grants and Programs Finder lists hundreds of active schemes across federal and state levels.

- Most government-backed loans offer below-market interest rates or zero-interest periods — but they come with strict eligibility rules and slow turnaround times.

- Export-focused businesses can access specialist support through Austrade's EMDG scheme and Export Finance Australia.

- State governments run their own programs — NSW, VIC, QLD, WA, and SA all have active grant portals.

- Startups and established businesses are both eligible for some programs, but most grants favour businesses already trading.

- Women-owned and Indigenous businesses have access to dedicated funding streams.

- When government programs don't fit — wrong timing, wrong industry, too slow — private lenders like specialist finance partners can fill the gap fast.

What Exactly Are Government Business Loans in Australia?

Government business loans in Australia are funding products where a federal or state government body either directly lends money to businesses or guarantees a portion of a loan made by a participating bank. The key difference from a commercial loan is the terms: lower interest rates, longer repayment windows, or interest-free periods that a standard bank wouldn't offer.

These sit under the broader umbrella of Australian Government-Backed Business Loans: Grants, Subsidies and Support Programs, which also includes:

- Grants

- money you don't repay, awarded for specific purposes

- Subsidies

- government co-contributions that reduce your costs (e.g., energy efficiency upgrades)

- Concessional loans

- loans at below-market rates, often through a bank acting as the delivery partner

- Guarantees

- government backs part of your loan so the bank takes less risk

- Vouchers and rebates

- smaller amounts for specific services like digital tools or training

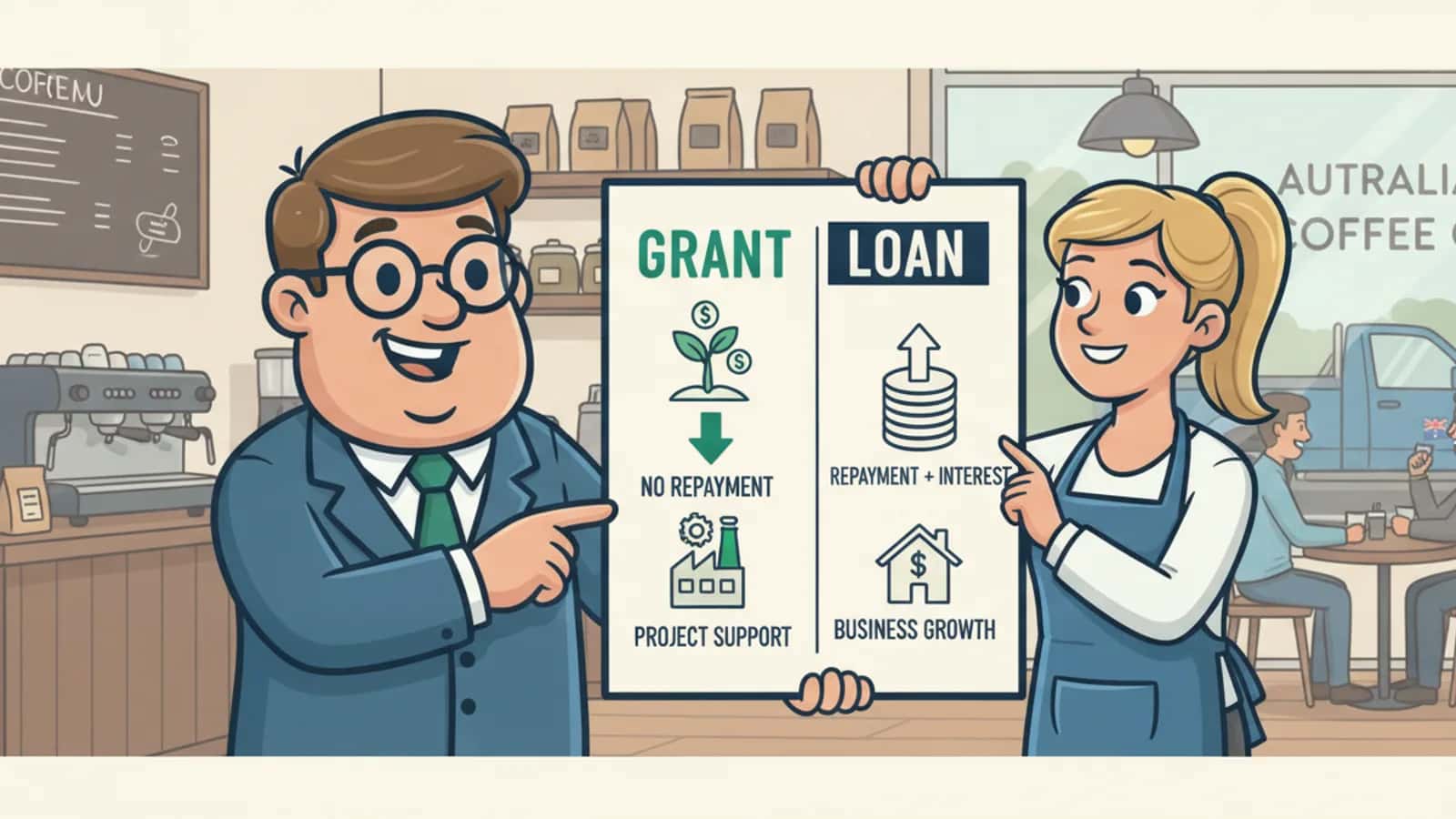

What's the Difference Between a Grant and a Loan?

A grant is funding you don't repay. A loan must be paid back, usually with interest. This sounds obvious, but many business owners apply for grants expecting cash in hand within weeks — and are surprised by the conditions attached.

| Feature | Grant | Government-Backed Loan |

|---|---|---|

| Repayment required? | ❌ No | ✅ Yes |

| Interest charged? | ❌ No | Usually low or zero |

| Competitive application? | ✅ Often | Sometimes |

| Restricted use of funds? | ✅ Usually strict | Varies |

| Processing time | Weeks to months | Weeks to months |

| Available to all businesses? | Rarely | Depends on program |

The practical rule: If you need cash to keep trading *now*, a grant is rarely the answer. The timelines are long and the criteria are narrow. A government-backed loan is faster but still slower than most private lenders. If speed matters, explore business funding options alongside your government applications.

How Do I Qualify for an Australian Small Business Grant?

Eligibility for Australian small business grants varies by program, but most share a common set of criteria. You generally need to meet *all* conditions — not just some.

Common eligibility requirements

- Registered ABN (active for a minimum period, often 12 months)

- Operate within a specific state, region, or industry

- Meet a turnover or employee count threshold (many programs cap at 200 employees)

- Use funds for an approved purpose (R&D, export, energy upgrades, hiring, etc.)

- Not have received the same grant previously

- Be able to co-fund a portion of the project (co-contribution is common)

The fastest way to find programs you actually qualify for is the Grants and Programs Finder on business.gov.au. Filter by business stage, industry, and location.

How Much Money Can I Actually Get from Australian Government Business Support?

The range is wide. Small voucher programs start at a few hundred dollars. Major concessional loans and export finance facilities can run into the millions.

Here's a rough breakdown by program type:

- State government vouchers and rebates:

- $500 – $25,000 (e.g., digital transformation vouchers, energy efficiency rebates)

- Federal business grants (e.g., R&D Tax Incentive, EMDG):

- $10,000 – $500,000+

- Export Market Development Grants (EMDG):

- Reimburses up to 50% of eligible export promotion expenses

- Concessional loans (e.g., Economic Resilience Program):

- Varies by program; zero-interest for up to two years

- Export Finance Australia:

- Loans, bonds, and guarantees for export businesses — amounts are project-specific

- Self-Employment Assistance Program:

- Supports individuals starting a business with training and small business planning support

The honest reality: Most small businesses receive modest amounts — a few thousand to tens of thousands. The large headline figures go to businesses with significant co-funding capacity, strong track records, and projects that align tightly with government priorities.

Are These Loans Good for Startups or Just Established Businesses?

Most government-backed loan and grant programs favour established businesses, not startups. This is one of the most common frustrations for early-stage founders.

Why established businesses get priority

- Programs require proof of trading history (often 12–24 months)

- Financial statements are needed to demonstrate viability

- Many grants require co-funding, which startups often can't provide

Startup-friendly exceptions

- The Self-Employment Assistance Program is specifically designed for people turning a business idea into a viable enterprise

- Some state programs offer small grants for new businesses in priority sectors

- The R&D Tax Incentive can benefit early-stage tech businesses with qualifying expenditure

Which is right for you?

Choose government programs if

You've been trading for at least 12 months, have a specific project in mind, and can wait 4–12 weeks for an outcome.

Choose a private lender if

You're early-stage, need capital quickly, or your business doesn't fit a narrow program category. See the full guide to business loans in Australia for a comparison of private funding options.

Which Banks and Agencies Offer Government-Backed Business Loans?

Government-backed loans in Australia are delivered through a mix of government agencies and participating commercial banks.

Federal delivery partners

- Export Finance Australia — direct lender and guarantor for export businesses

- ANZ, NAB, CBA, Westpac — participating banks for programs like the Economic Resilience Program

- Austrade — administers the EMDG scheme

- Department of Employment and Workplace Relations — Self-Employment Assistance

State-level delivery

- Service NSW — business grants, vouchers, and rebates

- Business Victoria, Business Queensland, Small Business Development Corporation (WA) — each state has its own portal and programs

The bank you use doesn't always matter — what matters is whether the program is open, whether you're eligible, and whether you apply before the funding round closes.

Do These Programs Work for Different Industries Like Tech or Agriculture?

Yes, but the fit varies significantly by industry. Australian Government-Backed Business Loans: Grants, Subsidies and Support Programs are not one-size-fits-all — many are designed for specific sectors.

Well-supported industries

- Agriculture: Farm Management Deposits, drought assistance, rural concessional loans

- Technology/R&D: R&D Tax Incentive, innovation grants, commercialisation programs

- Export businesses: EMDG, Export Finance Australia

- Energy and sustainability: Grants for renewable energy investment and efficiency upgrades

- Manufacturing: Various state-level support for capital investment

Less well-served industries

- Hospitality, retail, and personal services often find fewer targeted programs

- Construction and trades businesses may qualify for state-level programs but have fewer federal options

Practical tip: Search business.gov.au using your ANZSIC industry code for the most accurate program matches.

Are There Special Loans for Women-Owned or Indigenous Businesses?

Yes. Both the federal government and state governments run dedicated programs for underrepresented business owners.

For women-owned businesses

- The Boosting Female Founders Initiative provides grants to female-founded startups (check business.gov.au for current rounds)

- Some state programs include gender-specific eligibility criteria

For Indigenous businesses

- Indigenous Business Australia (IBA) provides concessional loans, equity investment, and business support specifically for Aboriginal and Torres Strait Islander entrepreneurs

- The New Leaf Enterprise and similar programs offer mentoring alongside funding

These programs often have less competition than mainstream grants, and the eligibility criteria are more focused on community and cultural outcomes than purely financial metrics.

What Are the Most Common Mistakes When Applying for Business Grants?

Most rejections are avoidable. The same errors come up repeatedly across grant applications.

Top mistakes:

- 1

Applying for a closed round

many programs run in funding rounds with hard deadlines. Check the status before investing time.

- 2

Missing a single eligibility criterion

if the program requires 12 months of trading and you have 11, you're out.

- 3

Vague project descriptions

grant assessors want specific outcomes, timelines, and budgets. "Grow my business" won't cut it.

- 4

Underestimating co-funding requirements

if a grant requires you to match 50% of the project cost, make sure you have that cash ready.

- 5

Applying for the wrong program

a loan application submitted to a grant program (or vice versa) wastes everyone's time.

- 6

Not keeping records

many programs require acquittal reports after funding is received. Poor record-keeping can affect future applications.

How Long Does the Application Process Typically Take?

Government business funding is slow. That's the honest answer. Most applicants wait weeks to months from application to decision.

Typical timelines

- Small state vouchers and rebates: 2–6 weeks

- Federal grants (competitive rounds): 6–16 weeks

- Concessional loans through banks: 4–10 weeks

- Export Finance Australia facilities: 6–12+ weeks

These timelines assume your application is complete and correct. Incomplete applications add weeks of back-and-forth.

If you need capital in days, not months, government programs are the wrong tool. Private specialist lenders can fund in 24–72 hours for businesses with solid revenue. A 2-minute eligibility check with no hard credit search is a practical first step while you wait on a government application.

What Kind of Businesses Usually Get Rejected for These Loans?

Rejections are common. Understanding why helps you avoid the same outcome.

Businesses that frequently get rejected

- Too new: Under 12 months trading, no financial history

- Wrong industry: Applying to a sector-specific program outside your ANZSIC code

- Poor financial records: No BAS, incomplete tax returns, or inconsistent revenue data

- Over the size threshold: Some programs cap at 20 employees; others at 200

- Already received the grant: Many programs have a "once only" rule

- Project doesn't fit the program purpose: Buying equipment under a marketing grant, for example

What happens if you can't repay a government business loan? Most programs have hardship provisions, but defaulting on a government loan has real consequences — it can affect future grant eligibility and, in some cases, trigger debt recovery through the ATO. Contact the program administrator early if repayment becomes difficult. Don't wait for a default notice.

Are There COVID-Related Business Support Programs Still Available in 2026?

Most COVID-specific business support programs — JobKeeper, the Cashflow Boost, and state-based COVID grants — have now closed. As of 2026, the emergency-era programs are no longer active.

What replaced them

- The Economic Resilience Program was introduced in response to more recent global disruptions (including Middle East conflict-related fuel cost impacts), offering zero-interest loans through participating banks like ANZ

- State governments continue to run general business resilience and recovery grants for businesses affected by natural disasters and economic shocks

- The business.gov.au grants finder is the most reliable place to check what's currently open

If a website is still advertising COVID-specific grants in 2026, verify the program status directly with the administering agency before spending time on an application.

When Government Programs Don't Move Fast Enough

Government funding is valuable — but it's not always available when you need it. Rounds close. Applications take months. Eligibility criteria rule out more businesses than they include.

That's where specialist private lenders come in. Platforms like Funding Fred connect Australian businesses with a panel of selected Australian finance partners — no big-four bank delays, no hard credit search to start.

Here's the practical comparison:

| Factor | Government Programs | Funding Fred |

|---|---|---|

| Decision time | Weeks to months | Often 24–72 hours |

| Paperwork | Extensive | Minimal |

| Credit criteria | Strict | Flexible, all credit types |

| Loan range | Varies by program | $5k – $7.5m |

| Hard credit check | Sometimes | No hard check to start |

| Obligation to proceed | No | No obligation |

Decision time

- Government Programs

- Weeks to months

- Funding Fred

- Often 24–72 hours

Paperwork

- Government Programs

- Extensive

- Funding Fred

- Minimal

Credit criteria

- Government Programs

- Strict

- Funding Fred

- Flexible, all credit types

Loan range

- Government Programs

- Varies by program

- Funding Fred

- $5k – $7.5m

Hard credit check

- Government Programs

- Sometimes

- Funding Fred

- No hard check to start

Obligation to proceed

- Government Programs

- No

- Funding Fred

- No obligation

Business Funding. Made Simple. A 2-minute eligibility check covers unsecured loans and merchant cash advances. Smart Matching connects you with the right specialist partner for your industry and revenue profile — whether you're a Sydney cafe, a Brisbane tradie, or a Perth retail store.

Check Eligibility Now — no hard check, no obligation.

Conclusion

Australian Government-Backed Business Loans: Grants, Subsidies and Support Programs offer real value — but only if you match the right program to your situation. Grants are competitive and slow. Government-backed loans are cheaper than commercial rates but come with strict criteria and long timelines. State programs add another layer of options worth exploring.

Actionable next steps:

- Search business.gov.au using your industry and state to find programs currently open

- Check your eligibility criteria carefully before investing time in an application

- Distinguish grants from loans — know whether you're applying for money you repay or money you keep

- If timing is urgent, explore private funding options alongside your government application — a 2-minute eligibility check costs nothing and has no hard credit impact

- Talk to your accountant about the R&D Tax Incentive and EMDG if you're in tech or export

For a broader look at Australian business loan options — including what private lenders actually look at — the Australian Business Loan Guides cover the full picture.

Government programs are one tool. They're not always the fastest or the most accessible. Knowing all your options means you're never stuck waiting.

Frequently asked questions

What Exactly Are Government Business Loans in Australia?

Government business loans in Australia are funding products where a federal or state government body either directly lends money to businesses or guarantees a portion of a loan made by a participating bank. The key difference from a commercial loan is the terms: lower interest rates, longer repayment windows, or interest-free periods that a standard bank wouldn't offer.

What's the Difference Between a Grant and a Loan?

A grant is funding you don't repay. A loan must be paid back, usually with interest. This sounds obvious, but many business owners apply for grants expecting cash in hand within weeks — and are surprised by the conditions attached.

How Do I Qualify for an Australian Small Business Grant?

Eligibility for Australian small business grants varies by program, but most share a common set of criteria. You generally need to meet *all* conditions — not just some.

How Much Money Can I Actually Get from Australian Government Business Support?

The range is wide. Small voucher programs start at a few hundred dollars. Major concessional loans and export finance facilities can run into the millions.

Are These Loans Good for Startups or Just Established Businesses?

Most government-backed loan and grant programs favour established businesses, not startups. This is one of the most common frustrations for early-stage founders.

Which Banks and Agencies Offer Government-Backed Business Loans?

Government-backed loans in Australia are delivered through a mix of government agencies and participating commercial banks.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Sources

- [1] Government Economic Resilience Program

- [2] Grants And Programs

- [3] Find Export Grants And Financial Assistance

- [4] Self Employment Assistance Data

- [5] Business Longitudinal Analysis Data Environment Blade

- [6] Business Grants

- [7] Grants And Funding

- [8] business.gov.au

- [9] Choose Your Funding

- [10] Grants And Support