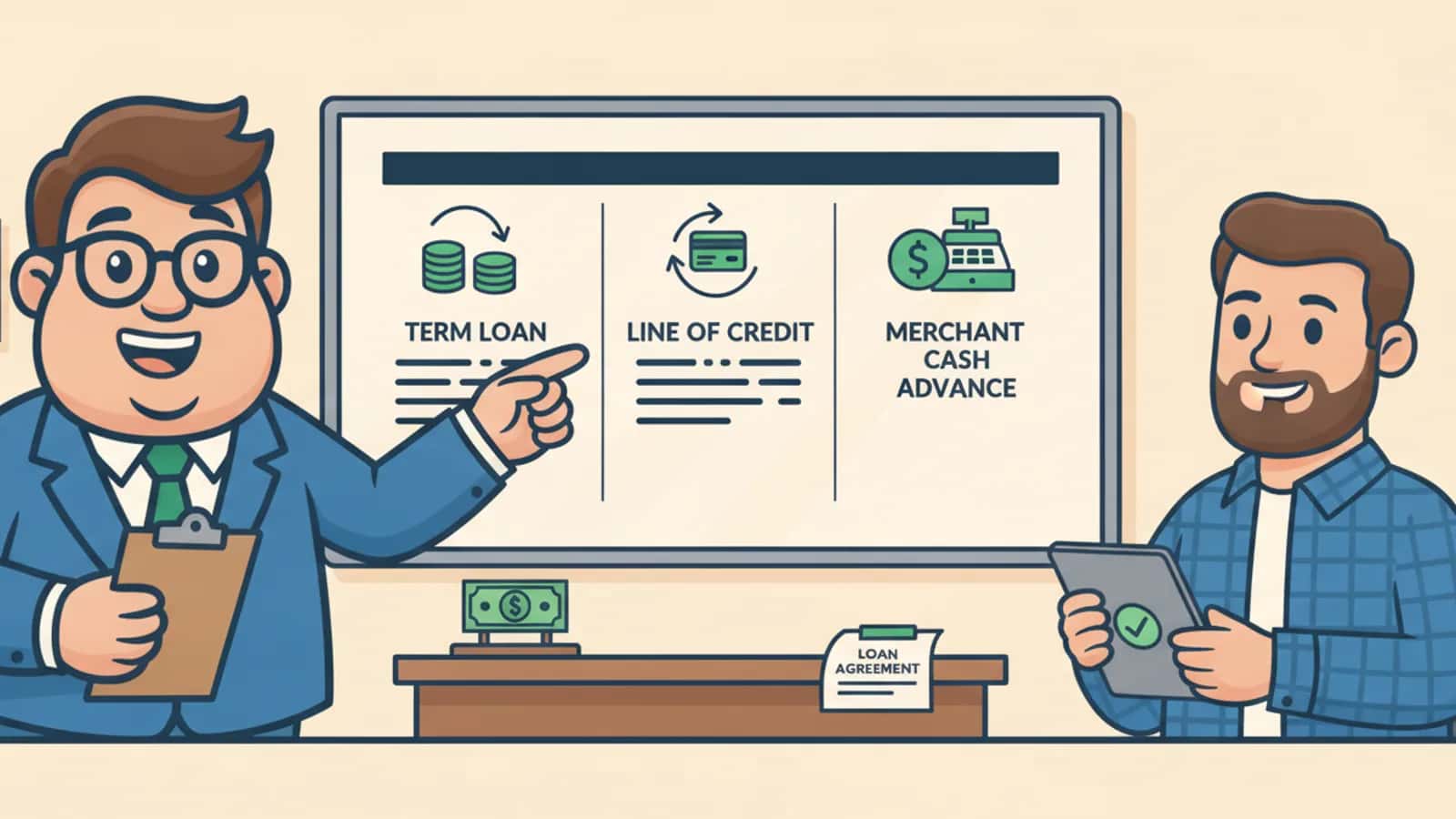

Term Loan vs Line of Credit vs Merchant Cash Advance: US Small Business Funding Compared

Term loans provide a lump sum upfront for long-term investments, lines of credit offer flexible access to funds as needed, and merchant cash advances deliver fast cash based on future sales.

Quick answer

Term loans provide a lump sum upfront for long-term investments, lines of credit offer flexible access to funds as needed, and merchant cash advances deliver fast cash based on future sales. The right choice depends on your cash flow needs, credit profile, and how quickly you need funding — with term loans best for major purchases, lines of credit ideal for ongoing expenses, and merchant cash advances suited for businesses needing immediate capital despite credit challenges.

Key takeaways

- Term loans work best for one-time investments like equipment or expansion, offering fixed payments over 1-10 years

- Lines of credit provide flexible working capital for ongoing expenses, charging interest only on funds used

- Merchant cash advances deliver funding fastest (24-48 hours) but cost the most, taking a percentage of daily sales

- Interest rates range from 6-45% for term loans, 8-60% for credit lines, and factor rates of 1.1-1.5 for cash advances

- Credit requirements vary significantly — term loans need the strongest credit, cash advances accept the weakest

- Seasonal businesses often benefit most from lines of credit due to flexible draw-down and repayment

- Fast eligibility checks help identify realistic options without hard credit pulls or extensive paperwork

What Exactly Is a Term Loan and How Does It Work

A term loan provides a lump sum of capital upfront, which you repay over a fixed period with regular monthly payments that include both principal and interest. The loan term typically ranges from one to ten years, making it suitable for long-term business investments like equipment purchases, real estate, or major expansion projects.

The application process requires detailed financial documentation including tax returns, bank statements, and business plans. Lenders evaluate your credit score, cash flow, and debt-to-income ratio before approval. Once approved, you receive the full amount immediately and begin making fixed payments regardless of whether you've used all the funds.

Key characteristics of term loans

- Fixed repayment schedule with predictable monthly payments

- Lower interest rates compared to other business funding options

- Longer approval process, often taking days to weeks

- Suitable for purchases with clear ROI projections

- May require collateral for larger amounts or riskier borrowers

Choose a term loan when you need a specific amount for a defined purpose and can handle fixed monthly payments. Avoid term loans for ongoing operational expenses or when you're unsure about the exact funding amount needed.

How Business Lines of Credit Function

A business line of credit works like a business credit card, providing access to funds up to a predetermined limit that you can draw from as needed. You only pay interest on the amount you actually use, and as you repay the borrowed funds, your available credit replenishes for future use.

Most business lines of credit offer terms up to five years with variable interest rates. You can access funds through online transfers, checks, or a linked debit card. This flexibility makes credit lines ideal for managing cash flow gaps, seasonal inventory purchases, or unexpected expenses.

How credit lines differ from term loans

- Pay interest only on funds drawn, not the entire credit limit

- Revolving credit that replenishes as you repay

- No fixed monthly payment amount — varies based on usage

- Faster approval process than term loans

- Higher interest rates but greater flexibility

The Federal Reserve's 2025 Small Business Credit Survey found that 52% of small businesses sought lines of credit, making them the most popular financing option. This popularity stems from their flexibility and the ability to have funds available before you need them.

Understanding Merchant Cash Advances

Merchant cash advances provide a lump sum payment in exchange for a percentage of your future credit card and debit card sales. Instead of fixed monthly payments, the advance is repaid through daily or weekly automatic deductions from your business bank account based on your sales volume.

MCAs use factor rates (typically 1.1 to 1.5) rather than traditional interest rates. A factor rate of 1.3 means you'll repay $1,300 for every $1,000 advanced. The actual cost depends on how quickly you repay — faster repayment reduces the total cost, while slower sales extend the repayment period and increase costs.

MCA characteristics

- Funding available within 24-48 hours

- No fixed repayment schedule — tied to sales volume

- Higher costs than traditional loans

- Minimal credit requirements

- Best suited for businesses with consistent card sales

Merchant cash advances work well for restaurants, retail stores, and service businesses that process significant credit card transactions. However, the daily payment structure can strain cash flow during slow periods, making them less suitable for businesses with irregular sales patterns.

Which Business Funding Option Is Cheapest for Startups

Term loans typically offer the lowest cost for startups with strong credit and established revenue, with rates starting around 6% for well-qualified borrowers. However, most startups struggle to qualify for traditional term loans due to limited operating history and insufficient collateral.

Lines of credit often provide the most cost-effective solution for startups needing flexible access to capital. While rates range from 8-60%, you only pay interest on funds used, making them cheaper than term loans when you don't need the full amount immediately.

Cost comparison for startups:

Term Loan

- Best Case Rate

- 6-12%

- Startup Reality

- Often unavailable

- When Cheapest

- Strong credit + 2+ years revenue

Line of Credit

- Best Case Rate

- 8-25%

- Startup Reality

- 15-35% typical

- When Cheapest

- Flexible usage needs

Merchant Cash Advance

- Best Case Rate

- Factor 1.1-1.2

- Startup Reality

- Factor 1.3-1.5

- When Cheapest

- Poor credit, fast need

For startups with revenue under $100,000 annually, merchant cash advances may be the only available option despite higher costs. The key is matching the funding type to your actual qualification profile rather than assuming you'll get the best advertised rates.

Consider using US business funding platforms that offer fast eligibility checks to understand realistic options before committing to applications that might damage your credit score.

Typical Interest Rates for Each Funding Type

Interest rates vary significantly based on your credit profile, business revenue, and industry risk factors. Term loans generally offer the lowest rates for qualified borrowers, while merchant cash advances carry the highest effective costs.

Term loan rates: 6% to 45% annually, with most small businesses paying 10-25%. SBA-backed term loans offer rates as low as 6-8% but require extensive documentation and longer approval times. Alternative lenders charge 15-45% but provide faster decisions and more flexible criteria.

Line of credit rates: 8% to 60% annually, with variable rates that can change based on market conditions. Secured lines backed by collateral typically offer better rates than unsecured options. Bank lines start around 8-15% for strong borrowers, while alternative lenders charge 20-60%.

Merchant cash advance costs: Factor rates of 1.1 to 1.5, translating to effective annual rates of 40-400% depending on repayment speed. A factor rate of 1.3 repaid over six months equals roughly 60% APR, while the same rate repaid over three months approaches 120% APR.

The actual rate you receive depends heavily on your business's financial profile. Revenue-led matching systems can help identify lenders most likely to offer competitive rates based on your specific situation and industry.

Credit Requirements: Do You Need Good Credit

Credit requirements vary dramatically across funding types, with term loans demanding the strongest credit profiles and merchant cash advances accepting the weakest. Understanding these differences helps you target appropriate options and avoid wasted applications.

Term loan credit requirements

- Personal credit score of 650+ for most lenders

- Business credit score of 75+ preferred

- Two years of business operation minimum

- Strong cash flow and debt service coverage

- Detailed financial documentation required

Line of credit credit requirements

- Personal credit score of 600+ for alternative lenders

- Some secured options available with scores as low as 550

- One year of business operation typical minimum

- Consistent revenue and bank account activity

- Less documentation than term loans but more than MCAs

Merchant cash advance credit requirements

- Personal credit scores as low as 400-500 accepted

- Business credit not typically required

- Three months of business operation sufficient

- Primary focus on credit card processing volume

- Bank statements often the only documentation needed

Bad credit doesn't eliminate all options, but it does limit you to higher-cost alternatives. Focus on improving your credit score over time while using available funding to grow revenue and strengthen your overall financial profile.

How Much Can You Qualify For

Qualification amounts depend on your business revenue, credit profile, and the specific funding type. Most lenders use revenue-based formulas to determine maximum funding levels, though other factors influence the final decision.

Term loan amounts

- Typically 10-30% of annual revenue

- $25,000 to $500,000 most common range

- SBA loans up to $5 million available

- Collateral may increase available amounts

- Industry and business model affect limits

Line of credit amounts

- Usually 10-20% of annual revenue

- $10,000 to $250,000 typical range

- Secured lines may offer higher limits

- Usage history affects future increases

- Seasonal businesses may get higher multiples

Merchant cash advance amounts

- Based on monthly credit card processing volume

- Typically 1-3 months of processing volume

- $5,000 to $500,000 range

- Daily sales volume determines repayment ability

- Multiple advances possible but not recommended

A business with $500,000 annual revenue might qualify for a $150,000 term loan, $100,000 line of credit, or $50,000 merchant cash advance, depending on their credit and cash flow situation. Smart matching systems consider these factors to show realistic qualification ranges before you apply.

Funding Speed Comparison

Funding speed often determines which option businesses choose, especially during cash flow emergencies or time-sensitive opportunities. Each funding type has different processing requirements that affect how quickly you can access capital.

Merchant cash advances: 24-48 hours from application to funding, making them the fastest option available. The streamlined approval process focuses primarily on credit card processing history rather than extensive financial analysis.

Lines of credit: Typically 2-7 days for approval and funding. Once established, additional draws are often available immediately or within hours. The initial setup takes longer, but ongoing access is nearly instant.

Term loans: Several days to weeks depending on the lender and loan amount. Traditional banks may take 30-90 days, while alternative lenders often complete the process in 1-2 weeks. SBA loans typically require 30-60 days due to additional government review.

Factors affecting speed

- Completeness of initial application

- Responsiveness to lender requests

- Complexity of business structure

- Loan amount and risk assessment

- Lender's internal processes and technology

When speed is critical, start with the fastest options but have backup plans. A merchant cash advance might solve immediate needs while you pursue a lower-cost term loan for longer-term requirements.

When to Choose Each Option

The right funding choice depends on your specific business needs, financial situation, and growth plans. Each option serves different purposes and works better in certain scenarios.

Which is right for you?

Choose term loans when

- Making a specific large purchase (equipment, real estate, acquisition)

- You need the lowest possible interest rate

- Cash flow can handle fixed monthly payments

- You have strong credit and financial documentation

- The investment has a clear return timeline

Choose lines of credit when

- Managing seasonal cash flow variations

- Covering ongoing operational expenses

- You want funds available before you need them

- Payment flexibility is important

- Building business credit history

Choose merchant cash advances when

- You need funding within 24-48 hours

- Traditional lenders have declined your application

- Credit card sales represent significant revenue

- Short-term need with quick repayment ability

- Other options aren't available due to credit issues

Many successful businesses use multiple funding types for different purposes. A restaurant might use a term loan for kitchen equipment, a line of credit for inventory management, and occasionally an MCA for emergency repairs.

Pros and Cons for Different Business Types

Different industries and business models benefit more from specific funding types based on their cash flow patterns, asset bases, and operational needs.

Restaurants and merchant cash advances: Restaurants often benefit from MCAs due to high credit card processing volumes, but the daily payment structure can strain operations during slow periods. The lack of collateral requirements helps newer restaurants that haven't built significant asset bases.

Pros: Fast funding, no collateral required, payments tied to sales volume Cons: High effective costs, daily payment pressure, can create cash flow stress during slow periods

Seasonal businesses and lines of credit: Businesses with seasonal revenue patterns like landscaping, retail, or tourism benefit most from lines of credit. They can draw funds during slow seasons and repay during peak periods without the pressure of fixed monthly payments.

Construction companies and term loans: Construction businesses often need term loans for equipment purchases and bonding requirements. The predictable payment structure works well with project-based revenue, and equipment can serve as collateral to secure better rates.

E-commerce and flexible funding: Online businesses might combine multiple funding types — lines of credit for inventory purchases, term loans for technology investments, and occasionally MCAs for marketing campaigns during peak seasons.

Consider your industry's typical cash flow patterns when evaluating options. What works for a steady service business may not suit a seasonal retailer or project-based contractor.

Repayment Challenges and Solutions

Understanding potential repayment difficulties helps you choose appropriate funding and prepare for challenges before they become critical problems.

What happens if you can't repay a business line of credit: Most credit lines allow interest-only payments during difficult periods, providing temporary relief while you stabilize cash flow. However, continued non-payment can result in the lender freezing your credit line, demanding immediate repayment, or pursuing legal action against personal guarantees.

Term loan repayment issues: Missing term loan payments typically triggers late fees and potential acceleration of the entire balance. Many lenders offer modification options including payment deferrals, term extensions, or temporary interest-only periods for borrowers experiencing temporary difficulties.

MCA repayment problems: Since MCAs are tied to daily sales, repayment automatically slows during poor sales periods. However, many agreements include minimum payment requirements that continue regardless of sales volume, potentially creating cash flow strain during extended slow periods.

Solutions for repayment difficulties

- Contact lenders immediately when problems arise

- Provide updated financial information and recovery plans

- Consider debt consolidation or refinancing options

- Explore business loan alternatives that better match your cash flow

- Work with financial advisors to restructure operations

Proactive communication with lenders often leads to better outcomes than waiting until payments are missed. Most lenders prefer working with borrowers to find solutions rather than pursuing collection actions.

Common Mistakes Small Businesses Make When Choosing Business Loans

Avoiding these frequent errors can save significant money and prevent funding problems that damage your business's financial health.

- 1

Choosing based on speed alone

Many businesses select merchant cash advances solely because they're fast, without considering the long-term cost impact. A $50,000 MCA with a 1.4 factor rate costs $70,000 to repay — $20,000 more than many term loans.

- 2

Not understanding true costs

Factor rates, origination fees, and variable interest rates can make funding much more expensive than initial quotes suggest. Always calculate the total repayment amount and effective annual percentage rate before deciding.

- 3

Borrowing more than needed

Term loans provide lump sums that start accruing interest immediately, even on unused portions. Lines of credit often make more sense when you're unsure about exact funding needs or timing.

- 4

Ignoring qualification reality

Applying for funding you're unlikely to qualify for wastes time and can damage your credit score through multiple hard inquiries. Use fast eligibility checks to understand realistic options first.

- 5

Not reading repayment terms

Daily payment requirements, personal guarantees, and acceleration clauses can create unexpected obligations. Understand exactly when and how you'll repay before signing agreements.

- 6

Stacking multiple high-cost advances

Taking multiple MCAs or short-term loans creates a debt spiral where daily payments consume increasing portions of revenue, making it harder to operate profitably.

Smart business owners compare total costs, match funding types to actual needs, and maintain realistic expectations about qualification requirements.

Legal Considerations Across US States

Merchant cash advances are legal in all US states, but regulations vary significantly regarding disclosure requirements, maximum costs, and collection practices. Understanding your state's rules helps protect your business from predatory practices.

Federal regulations: MCAs aren't technically loans, so they avoid many federal lending regulations. However, the Federal Trade Commission requires clear disclosure of terms, and the Consumer Financial Protection Bureau monitors industry practices for unfair or deceptive practices.

State-level variations

- New York requires detailed cost disclosures and caps on certain fees

- California has specific requirements for MCA agreements and collection practices

- Texas focuses on licensing requirements for MCA providers

- Florida has disclosure requirements but fewer cost restrictions

Key legal protections

- Right to receive clear terms before signing

- Protection against harassment during collection

- Ability to file complaints with state regulatory agencies

- Access to legal remedies for contract violations

Red flags indicating potential legal issues

- Refusal to provide written terms before funding

- Pressure to sign immediately without review time

- Threats of criminal prosecution for civil debt

- Attempts to access business accounts without authorization

Always review agreements with legal counsel when dealing with significant amounts or unfamiliar lenders. State attorney general offices often provide resources for businesses dealing with problematic lenders.

Next steps for term loan vs line of credit vs merchant cash advance us small business funding c

Choosing between term loans, lines of credit, and merchant cash advances depends on your specific business needs, credit profile, and cash flow situation. Term loans offer the lowest costs for major investments when you have strong credit and can handle fixed payments. Lines of credit provide flexible access to working capital for ongoing needs and seasonal businesses. Merchant cash advances deliver fast funding for businesses that can't qualify elsewhere, despite higher costs.

The key is matching funding types to your actual qualification profile and business needs rather than assuming you'll get the best advertised terms. Start with a realistic assessment of your credit, revenue, and documentation readiness.

Before committing to any funding option, use platforms that offer fast eligibility checks to understand what you might qualify for across multiple lenders without hard credit pulls. This approach helps you compare realistic options and avoid applications that could damage your credit score.

Remember that business funding is a tool to grow revenue and improve operations. Choose options that support your business goals without creating unsustainable payment obligations that could harm your long-term success.

Further reading

Frequently asked questions

What Exactly Is a Term Loan and How Does It Work?

A term loan provides a lump sum of capital upfront, which you repay over a fixed period with regular monthly payments that include both principal and interest. The loan term typically ranges from one to ten years, making it suitable for long-term business investments like equipment purchases, real estate, or major expansion projects.

How Business Lines of Credit Function?

A business line of credit works like a business credit card, providing access to funds up to a predetermined limit that you can draw from as needed. You only pay interest on the amount you actually use, and as you repay the borrowed funds, your available credit replenishes for future use.

Which Business Funding Option Is Cheapest for Startups?

Term loans typically offer the lowest cost for startups with strong credit and established revenue, with rates starting around 6% for well-qualified borrowers. However, most startups struggle to qualify for traditional term loans due to limited operating history and insufficient collateral.

How Much Can You Qualify For?

Qualification amounts depend on your business revenue, credit profile, and the specific funding type. Most lenders use revenue-based formulas to determine maximum funding levels, though other factors influence the final decision.

When to Choose Each Option?

The right funding choice depends on your specific business needs, financial situation, and growth plans. Each option serves different purposes and works better in certain scenarios.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Sources

- Small Business Line Of Credit Vs Term Loan [2] Terms - https://www.nerdwallet.com/business/loans/learn/terms [3] How Do Business Loans Work - https://www.forbes.com/advisor/business-loans/how-do-business-loans-work/ [4] Business Loan Vs Line Of Credit - https://www.bankrate.com/loans/small-business/business-loan-vs-line-of-credit/ [5] Merchant Cash Advance - https://zetbanker.com/us/article/merchant-cash-advance

- U.S. Small Business Administration loans

- U.S. Treasury small business programs