Online vs Bank Business Loans in Australia: Which Is Better for Your SME in 2026?

For most Australian SMEs that need capital quickly, online lenders win on speed, flexibility, and accessibility — especially if your credit file isn't perfect or your business is under three years old. Traditional banks still make sense for large, long-term loans where you can wait weeks and have strong financials to back you up.

Quick answer

For most Australian SMEs that need capital quickly, online lenders win on speed, flexibility, and accessibility — especially if your credit file isn't perfect or your business is under three years old. Traditional banks still make sense for large, long-term loans where you can wait weeks and have strong financials to back you up. The right choice depends on how fast you need funds, how much documentation you can provide, and what your credit profile looks like right now.

Key takeaways

- Banks typically take 2 to 6 weeks to approve a business loan; online lenders can approve and fund in 1 to 3 business days

- Bank approval rates for small business loans at major institutions sit between just 13% and 22%

- Online lenders may accept credit scores as low as 550 and businesses trading for as little as 12 months

- Bank interest rates generally run 6%–12% APR; online lender rates range from 10% to over 40% depending on risk profile

- New lending to Australian SMEs grew from AUD $122.5 billion in 2023 to AUD $153.7 billion in 2024, showing strong demand

- Non-bank lenders are capturing a growing share of SME loan originations in Australia

- Online loans suit working capital, equipment, and short-term growth needs; banks suit large property-secured, long-term funding

- Platforms like Funding Fred run a 2-minute eligibility check with no hard credit search to start — so you can compare options without risk

What's the Difference Between Online and Traditional Bank Business Loans?

Online business loans and traditional bank loans both put capital in your hands — but the process, criteria, and speed are very different. Banks are structured for low-risk, high-documentation lending. Online lenders are built for speed and flexibility, assessing your actual business performance rather than just your credit file.

Here's how they compare side by side:

| Feature | Traditional Bank | Online Lender (e.g. via Funding Fred) |

|---|---|---|

| Approval time | 2–6 weeks | 1–3 business days |

| Interest rate | 6%–12% APR | 10%–40%+ APR |

| Min. credit score | ~680 | From ~550 |

| Min. trading history | 2–3 years | 12 months |

| Documentation | Extensive (tax returns, financials, property) | Minimal (bank statements, ABN, ID) |

| Loan amounts | $25k–$5m+ | $5k–$7.5m |

| Repayment terms | 1–10 years | 3–24 months |

| Collateral required | Often yes | Often no (unsecured options available) |

| Hard credit check upfront | Yes | Not always — Funding Fred starts with no hard check |

Approval time

- Traditional Bank

- 2–6 weeks

- Online Lender (e.g. via Funding Fred)

- 1–3 business days

Interest rate

- Traditional Bank

- 6%–12% APR

- Online Lender (e.g. via Funding Fred)

- 10%–40%+ APR

Min. credit score

- Traditional Bank

- ~680

- Online Lender (e.g. via Funding Fred)

- From ~550

Min. trading history

- Traditional Bank

- 2–3 years

- Online Lender (e.g. via Funding Fred)

- 12 months

Documentation

- Traditional Bank

- Extensive (tax returns, financials, property)

- Online Lender (e.g. via Funding Fred)

- Minimal (bank statements, ABN, ID)

Loan amounts

- Traditional Bank

- $25k–$5m+

- Online Lender (e.g. via Funding Fred)

- $5k–$7.5m

Repayment terms

- Traditional Bank

- 1–10 years

- Online Lender (e.g. via Funding Fred)

- 3–24 months

Collateral required

- Traditional Bank

- Often yes

- Online Lender (e.g. via Funding Fred)

- Often no (unsecured options available)

Hard credit check upfront

- Traditional Bank

- Yes

- Online Lender (e.g. via Funding Fred)

- Not always — Funding Fred starts with no hard check

The core trade-off: banks are cheaper if you qualify, but most SMEs don't clear the bar. Online lenders cost more but actually say yes.

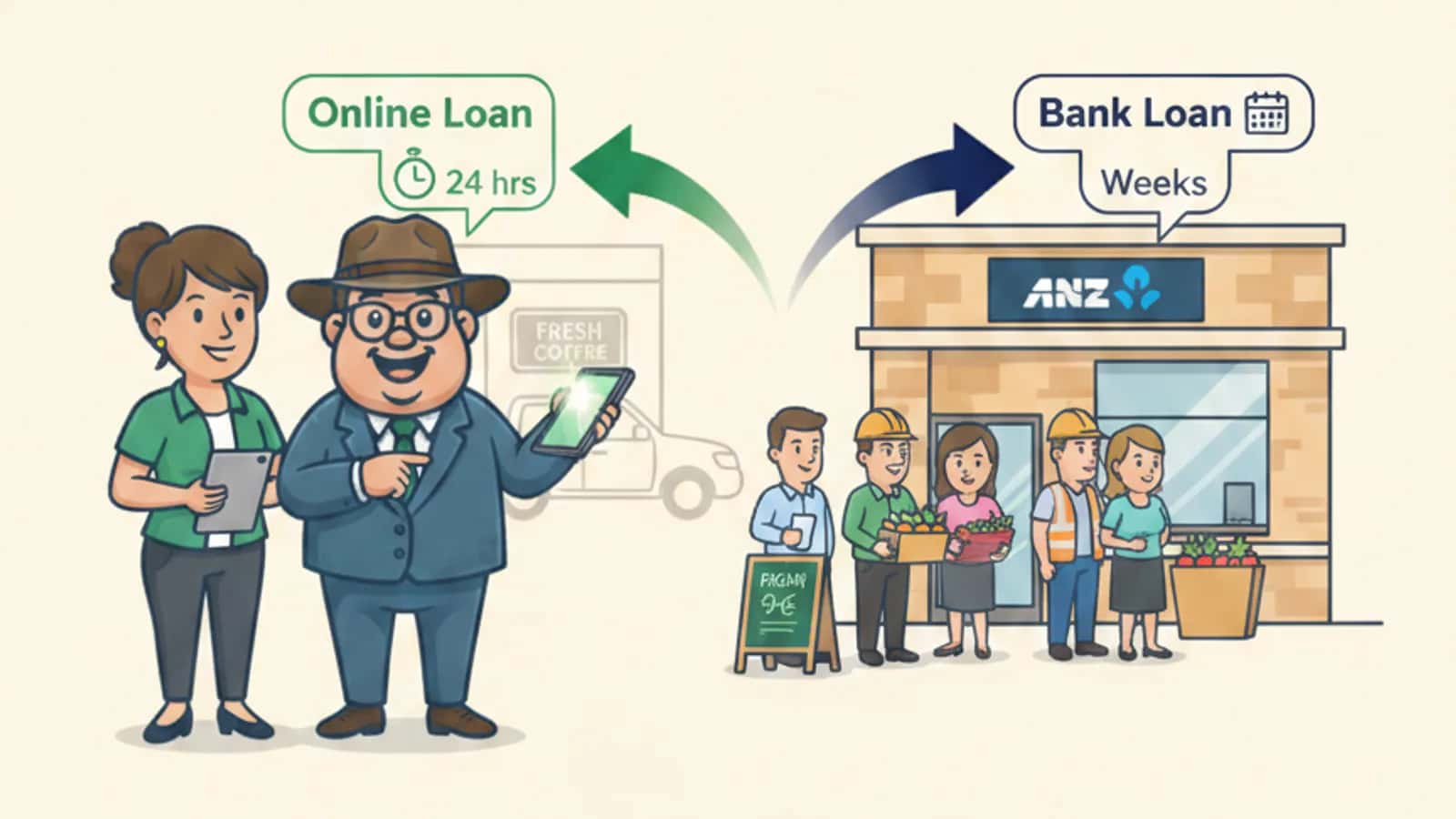

How Much Faster Can You Get Approved for an Online Loan Compared to a Bank?

Online lenders can approve and fund a business loan in 1 to 3 business days. Banks typically take 2 to 6 weeks from application to settlement.

That's not a minor difference. If a Melbourne café owner needs to replace a commercial fridge before the weekend, a bank timeline isn't a real option. An online lender can have funds in the account by Thursday if you apply Tuesday afternoon.

The speed gap comes down to process:

- Banks

- require in-person meetings, manual document review, credit committee sign-off, and often a property valuation

- Online lenders

- use automated decisioning, open banking data, and digital ID verification — the whole thing runs faster because it's built to

For businesses needing working capital, seasonal stock, or emergency repairs, speed isn't a nice-to-have. It's the whole point.

Which Loan Type Has Lower Interest Rates in Australia Right Now?

Banks offer lower rates — typically 6% to 12% APR — compared to online lenders, which range from 10% to over 40% depending on your risk profile. But the rate comparison only matters if you can actually get approved for the bank loan.

A few things to keep in mind:

- Bank rates are lower but conditional.

- You need a strong credit score, years of trading history, and often property as security to access those rates.

- Online rates reflect risk and speed.

- A higher rate on a short-term unsecured loan may still be cheaper than the cost of missing a business opportunity.

- Comparison rates matter more than headline rates.

- Always check fees, early repayment penalties, and whether the rate is flat or reducing. See our guide on how to compare business loan rates and fees for a full breakdown.

Which is right for you?

Choose a bank if

You qualify, you're not in a hurry, and the loan is large enough that rate savings outweigh the wait.

Choose an online lender if

You need funds fast, your credit file isn't perfect, or the loan amount is under $500k and you want an answer this week.

Are Online Business Loans Safe for Small Australian Companies?

Yes — reputable online lenders operating in Australia are regulated under the Australian Securities and Investments Commission (ASIC) and must comply with the National Consumer Credit Protection Act and relevant financial services licensing requirements. The industry has matured significantly, with established non-bank lenders now accounting for a growing share of SME lending nationally.

To stay safe:

- Check the lender holds an Australian Credit Licence (ACL) or is credit-licensed through an authorised representative

- Read the loan contract carefully — especially fees, repayment structure, and default terms

- Use a platform that connects you to selected Australian finance partners with verified credentials

- Avoid any lender that asks for upfront fees before approval

Funding Fred connects SMEs with specialist partners who meet Australian regulatory standards. No obligation to proceed after your 2-minute check.

What Credit Score Do You Need for an Online Business Loan?

Online lenders typically accept credit scores from around 550, compared to the 680+ most banks require. Some online lenders place more weight on revenue and cash flow than on credit score alone.

That said, a lower score will affect your rate. Here's what lenders actually look at:

- Revenue and monthly turnover

- consistent cash flow matters more than a perfect score

- Trading age

- most online lenders want at least 6–12 months of trading history

- Outstanding defaults or bankruptcies

- these are assessed case by case; some lenders specialise in this area

- Industry type

- some sectors are considered higher risk regardless of credit score

If your credit history has bumps, it's worth reading our guide on bad credit business loans in Australia before you apply. There are practical steps you can take to strengthen your application even before you submit.

Which Loan Type Is Better for Startups with Limited Financial History?

Online lenders are almost always the better option for startups. Banks typically require 2 to 3 years of trading history and full financial statements. Most startups simply don't have that yet.

Online lenders are more likely to consider:

- Businesses trading for 6–12 months

- Revenue-based assessments rather than years of tax returns

- Merchant cash advances tied to card sales volume — useful for retail and hospitality startups

- Unsecured loans based on projected cash flow and bank statement history

For startups with no track record at all, the options narrow further — but they do exist. See our detailed breakdown of business loans for startups in Australia for what's actually available and how to position your application.

What Are the Hidden Fees in Online vs Bank Business Loans?

Both loan types carry fees beyond the headline interest rate — but they show up differently. Banks tend to charge establishment fees, ongoing account-keeping fees, and early repayment penalties. Online lenders may charge origination fees, risk fees, and factor rates that make the true cost harder to calculate at first glance.

Common fees to watch for:

| Fee Type | Bank Loans | Online Loans |

|---|---|---|

| Establishment/origination fee | 0.5%–2% of loan | 1%–5% of loan |

| Monthly account fee | Sometimes | Sometimes |

| Early repayment penalty | Common | Varies |

| Late payment fee | Yes | Yes |

| Valuation fee (if secured) | Often | Rare |

The safest approach: ask for the total cost of the loan in dollar terms, not just the rate. For a plain-language explanation of APR, flat rates, and comparison rates, our business loan terms explained guide is a good starting point.

Can You Get a Larger Loan Amount from a Bank or Online Lender?

Banks can lend larger amounts — typically $25,000 to $5 million or more — especially for property-secured lending. Online lenders have historically capped out lower, though platforms like Funding Fred now facilitate unsecured loans up to $7.5 million through specialist partners.

For most SMEs needing under $500,000, online lenders are competitive on amount and far ahead on speed. For loans above $1 million, especially those secured against commercial property, a bank or private lender relationship may still make sense — though the application process will be significantly longer.

Are Online Business Loans Good for Tradies and Construction Businesses?

Yes — online loans are well-suited to trades and construction businesses, which often have lumpy cash flow, seasonal demand, and urgent equipment needs that don't fit neatly into a bank's approval timeline.

A Brisbane concreting company waiting on a $40,000 equipment repair can't wait six weeks for a bank decision. An Adelaide plumbing business that wins a large contract and needs to hire two more staff immediately needs capital now, not next month.

Online lenders assess:

- Monthly revenue from bank statements

- ABN registration and trading age

- Type of work (residential, commercial, civil)

- Outstanding invoices or contract values

Unsecured loans and merchant cash advances both work well for trades. The commercial banker vs online business lender comparison goes deeper on this for trade-specific scenarios.

What Documents Do You Need to Apply for an Online Business Loan?

Most online lenders require far less paperwork than banks. A typical online application needs:

- ABN

- (active, registered in your name or your business name)

- 3–6 months of business bank statements

- (often via secure open banking connection)

- Government-issued photo ID

- (driver's licence or passport)

- Basic business details

- trading name, industry, monthly revenue estimate

Banks, by contrast, typically require:

- 2–3 years of tax returns (business and personal)

- Full profit and loss statements and balance sheets

- ATO portal access or BAS statements

- Property valuations (if secured)

- Detailed business plans for larger loans

The documentation gap is one of the biggest practical differences in the online vs bank business loans debate in Australia. For a full checklist of what lenders want, see the Australian business loan approval checklist.

How Do Repayment Terms Differ Between Online and Bank Loans?

Bank loans offer longer repayment terms — typically 1 to 10 years — which keeps monthly repayments lower but means you're paying interest for longer. Online loans run shorter — usually 3 to 24 months — with daily, weekly, or fortnightly repayments that align with cash flow cycles.

Which suits your situation

- Long-term bank loan — best for major capital investment (property, large equipment) where you need low monthly repayments over years

- Short-term online loan — best for working capital, stock purchase, marketing spend, or bridging a cash flow gap

- Merchant cash advance — repaid as a percentage of daily card sales, so repayments flex with revenue. Suits hospitality, retail, and e-commerce businesses with variable income

Which Loan Type Is Easier If You Have Bad Credit?

Online lenders are significantly more accessible for businesses with bad credit. Banks will typically decline any application below a 680 credit score. Online lenders and specialist non-bank lenders consider the full picture — revenue, trading history, sector, and cash flow — rather than leading with a credit score cut-off.

Key points for bad credit applicants:

- Some specialist lenders focus specifically on "all credit types" — including defaults and prior rejections

- Secured loans (against equipment or invoices) can offset credit risk

- Demonstrating consistent monthly revenue is often more persuasive than a clean credit history

- Applying through a matching platform avoids multiple hard credit checks that further damage your score

Funding Fred's 2-minute eligibility check uses no hard credit search to start — so checking your options won't affect your credit file.

What Happens If You Can't Repay an Online Business Loan?

Missing repayments on an online business loan triggers a process similar to any lender — but the specifics vary. Most lenders will:

- Contact you immediately and offer a hardship arrangement or repayment pause

- Apply late payment fees as set out in the loan contract

- Report the default to credit bureaus if unresolved (this affects future borrowing)

- Pursue recovery through a debt collector or legal action for larger amounts

- Enforce any security held (if the loan was secured against assets)

What to do if you're struggling

- Contact your lender before you miss a payment — most have hardship provisions

- Check whether ASIC's MoneySmart or the Australian Financial Complaints Authority (AFCA) can assist

- Don't take out a second loan to repay the first without getting advice first

The best protection is borrowing only what your cash flow can service. Use the business loan pre-approval guide to stress-test your repayment capacity before you commit.

Conclusion: Online vs Bank Business Loans in Australia — Making the Right Call for Your SME in 2026

The honest answer to "Online vs Bank Business Loans in Australia: Which Is Better for Your SME in 2026?" is: it depends on your timeline, your credit profile, and how much you need.

Go with a bank if you have strong financials, a clean credit file, 2+ years of trading history, and you're not in a hurry. The rates are better and the terms are longer.

Go with an online lender if you need funds in days not weeks, your credit file isn't perfect, you're a startup or early-stage business, or the loan amount is under $500,000 and you want a fast, low-friction process.

For most Australian SMEs — the café in Gold Coast, the tradie in Perth, the retail store in Adelaide, the e-commerce operator in Sydney — the bank process is too slow, too strict, and too document-heavy. Online lenders exist precisely because the major banks say no to a large proportion of viable small businesses.

Actionable next steps:

- Work out how much you need and when you need it

- Check your current credit score so you know where you stand

- Gather 3–6 months of bank statements — the minimum most online lenders need

- Run a 2-minute eligibility check through Funding Fred — no hard credit search, no obligation to proceed

- Compare offers from specialist partners before you commit

Business Funding. Made Simple. Check Eligibility Now — it takes two minutes and won't affect your credit file.

Further reading

Frequently asked questions

What's the Difference Between Online and Traditional Bank Business Loans?

Online business loans and traditional bank loans both put capital in your hands — but the process, criteria, and speed are very different. Banks are structured for low-risk, high-documentation lending. Online lenders are built for speed and flexibility, assessing your actual business performance rather than just your credit file.

How Much Faster Can You Get Approved for an Online Loan Compared to a Bank?

Online lenders can approve and fund a business loan in 1 to 3 business days. Banks typically take 2 to 6 weeks from application to settlement.

Which Loan Type Has Lower Interest Rates in Australia Right Now?

Banks offer lower rates — typically 6% to 12% APR — compared to online lenders, which range from 10% to over 40% depending on your risk profile. But the rate comparison only matters if you can actually get approved for the bank loan.

Are Online Business Loans Safe for Small Australian Companies?

Yes — reputable online lenders operating in Australia are regulated under the Australian Securities and Investments Commission (ASIC) and must comply with the National Consumer Credit Protection Act and relevant financial services licensing requirements. The industry has matured significantly, with established non-bank lenders now accounting for a growing share of SME lending nationally.

What Credit Score Do You Need for an Online Business Loan?

Online lenders typically accept credit scores from around 550, compared to the 680+ most banks require. Some online lenders place more weight on revenue and cash flow than on credit score alone.

Which Loan Type Is Better for Startups with Limited Financial History?

Online lenders are almost always the better option for startups. Banks typically require 2 to 3 years of trading history and full financial statements. Most startups simply don't have that yet.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Sources

- Online Business Lenders Vs Traditional Banks

- Online Lenders Vs Traditional Banks What Australian Smes Need To Know

- Bank Loan Vs Online Business Loan

- Business Loan Definition Australia 2026

- Australia Bdcad0cc

- Abn Business Loans Guide

- What Is Private Lending

- Business Lending Options In 2026 Whats Right For You

Related guides