Commercial Banker vs Online Business Lender: Which Is Better for Australian SMEs in 2026?

For most Australian SMEs that need capital fast, an online business lender will get money in your account days — not weeks — after applying, with less paperwork and more flexible criteria than a traditional commercial bank. But if you need a large, long-term facility and have a clean financial history, a commercial banker may still offer a lower rate.

Quick answer

For most Australian SMEs that need capital fast, an online business lender will get money in your account days — not weeks — after applying, with less paperwork and more flexible criteria than a traditional commercial bank. But if you need a large, long-term facility and have a clean financial history, a commercial banker may still offer a lower rate. The right answer depends on how urgently you need funds, your credit profile, and how much documentation you can realistically pull together.

Key takeaways

- Major Australian banks approve only 25–35% of SME loan applications under $1 million, with timelines of 21–35 days

- Online lenders can approve and fund within 24–72 hours, with higher approval rates for businesses trading 3+ years

- 34% of Australian SMEs now use non-bank lending for core business needs — and 92% have used or would consider a non-bank lender

- Bank rates for qualified borrowers typically sit at 6–12% APR; online lender rates range from 10–40% depending on risk profile

- New lending to Australian SMEs jumped from AUD 122.5 billion in 2023 to AUD 153.7 billion in 2024

- Online lenders assess actual business performance — revenue, trading history, sector — not just credit scores

- Businesses with credit scores below 680 are routinely declined by major banks but may still qualify online

- Hidden costs (establishment fees, early repayment penalties, factor rates) exist on both sides — always read the comparison rate

- Startups with under 12 months of trading history face the steepest barriers with commercial banks

- Platforms like Funding Fred run a 2 min check with no hard credit search to start — no obligation to proceed

What Exactly Does a Commercial Banker Do for Small Businesses?

A commercial banker is a relationship manager at a major or regional bank who assesses, structures, and manages business lending facilities. For Australian SMEs, this typically means term loans, overdrafts, trade finance, or commercial property lending — all assessed against the bank's internal credit policy.

The relationship model sounds appealing. In practice, it means:

- A dedicated contact

- who knows your business over time (useful for large, complex facilities)

- Credit assessment

- based on audited financials, tax returns, BAS statements, and personal assets

- Security requirements

- most bank loans under $500k still require real estate or other hard assets as collateral

- Longer terms

- 3 to 25 years, with monthly repayments

- Lower headline rates

- typically 6–12% APR for well-qualified borrowers

The catch? The process is built for businesses that already look great on paper. If your financials are messy, your credit history has a blemish, or you need money in less than a month, the commercial banking model works against you.

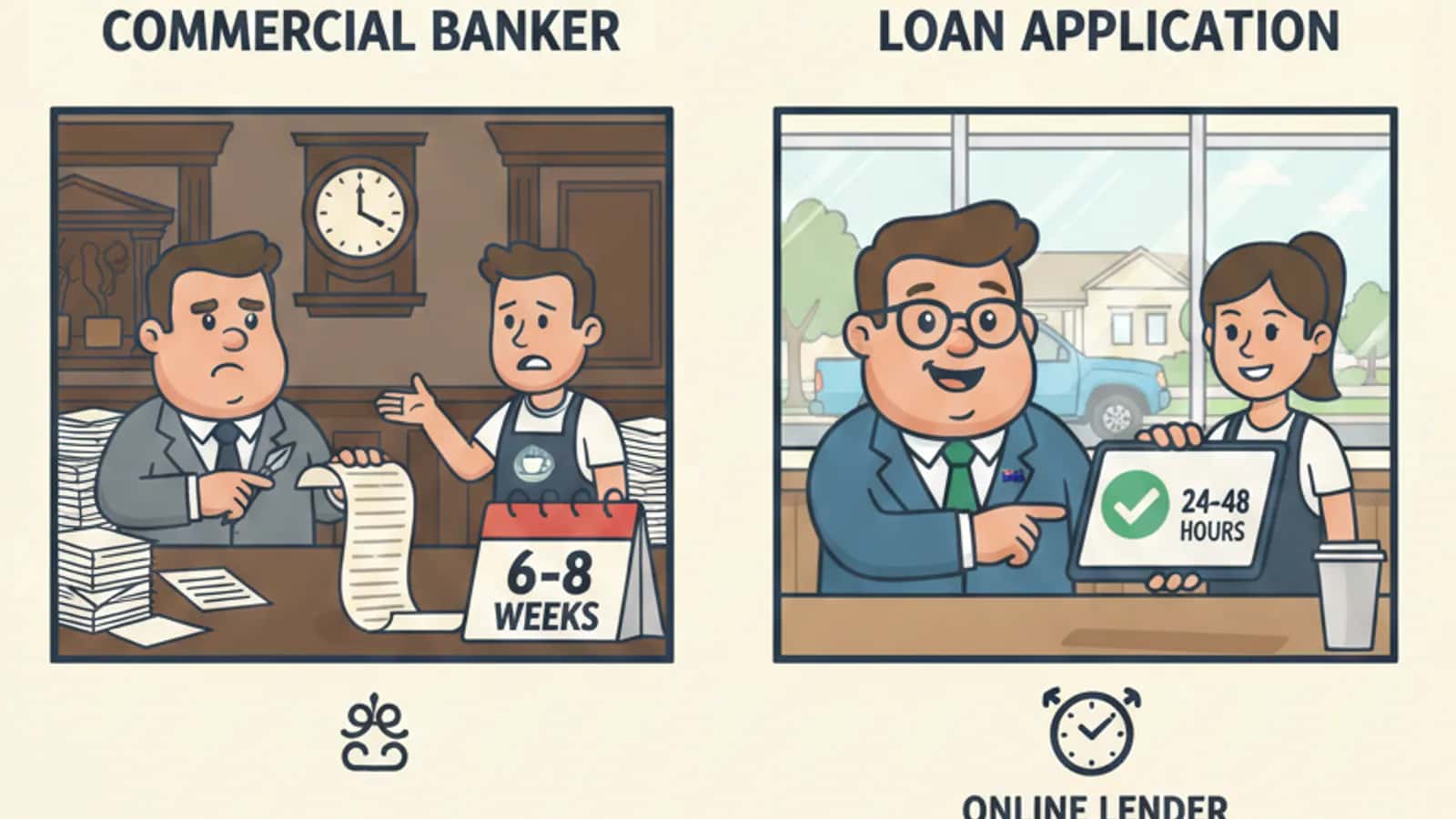

How Much Faster Are Online Business Loans Compared to Traditional Bank Loans?

Online lenders are dramatically faster — typically 24 to 72 hours from application to funding, compared to 21 to 35 days for major Australian banks.

That gap matters enormously in practice. A Melbourne café owner who needs to replace a commercial espresso machine before the weekend rush can't wait five weeks. A Gold Coast construction firm that wins a contract and needs to cover materials upfront can't afford a month of back-and-forth with a bank credit team.

Typical timelines side by side:

| Step | Commercial Bank | Online Lender |

|---|---|---|

| Initial application | 1–2 hours (in branch or portal) | 2 minutes (eligibility check) |

| Document collection | 3–10 business days | 1–2 business days |

| Credit assessment | 10–20 business days | Same day to 24 hours |

| Approval decision | 21–35 days total | 24–72 hours |

| Funds in account | Add 1–3 days post-approval | Often same day as approval |

The speed difference comes down to how each lender assesses risk. Banks rely on manual review of historical documents. Online lenders use automated data analysis — bank transaction feeds, accounting software integrations, and real-time revenue data — to make faster, smarter decisions.

What Are the Average Interest Rates: Commercial Bank vs Online Lender in Australia?

Banks generally offer lower headline rates (6–12% APR) for borrowers who qualify, while online lenders charge 10–40% or more depending on the risk profile. The OECD reported that interest rates on outstanding Australian SME loans averaged 6.6% in 2024.

But rate comparisons between bank and non-bank products are rarely apples-to-apples. Here's what actually affects the number you pay:

- Loan term:

- Bank loans run 3–25 years; online loans typically 3 months to 5 years. A shorter term at a higher rate can cost less total interest than a long-term bank loan

- Fee structures:

- Banks charge establishment fees, ongoing account fees, and sometimes early repayment penalties. Online lenders may use factor rates rather than APR — which changes how you calculate total cost

- Collateral:

- Unsecured online loans carry higher rates because the lender takes on more risk. Secured bank loans are cheaper but require assets

- Credit profile:

- A business with a 720 credit score and three years of clean financials will get a bank's best rate. Everyone else pays more — or gets declined

For a fair comparison, always look at the comparison rate and total cost of credit, not just the advertised interest rate. A detailed breakdown of how to do this is covered in our guide to comparing business loan rates and fees.

Can Small Businesses with Average Credit Still Get Approved Online?

Yes. Online lenders are built to assess businesses that don't fit the bank mould. While major banks typically require a credit score of 680 or above and 2–3 years of trading history, many online lenders will consider scores from 550 upward and businesses trading for as little as 6–12 months.

The key difference is how risk is assessed. Online lenders look at:

- Revenue consistency

- regular income from a verified bank feed matters more than a perfect credit file

- Trading age

- 12+ months is the typical minimum; 3+ years unlocks better rates

- Industry type

- some sectors (hospitality, construction, retail) are assessed differently based on sector-specific default data

- Cash flow patterns

- seasonal businesses can explain revenue dips with context that a bank's algorithm would simply flag as risk

If your credit history has had some bumps, it's worth reading our detailed guide on bad credit business loans in Australia before applying anywhere. Knowing what lenders actually look at helps you put your best case forward.

Choose online lending if: Your credit score is under 680, your business is under 2 years old, or you've had a late payment or default in the past 3 years.

Which Type of Lender Typically Offers Lower Fees — and What Hidden Costs Should You Watch For?

Banks tend to have lower interest rates but more complex fee structures. Online lenders are more transparent upfront but may use factor rates or daily repayment schedules that make total cost harder to calculate at a glance.

Watch for these costs on both sides

- Establishment/origination fees: 1–3% of the loan amount, charged upfront

- Ongoing account-keeping fees: More common with bank overdrafts and lines of credit

- Early repayment penalties: Banks often charge break costs on fixed-rate loans; some online lenders also penalise early payoff

- Factor rates (online lenders): A factor rate of 1.25 on a $50,000 loan means you repay $62,500 total — regardless of how quickly you pay it off

- Daily/weekly repayments: Shorter repayment cycles improve lender cash flow but can strain yours if revenue is uneven

The Australian Business Loan Terms Explained guide covers APR, comparison rates, and factor rates in plain language — worth a read before signing anything.

Are Online Business Loans Safe and Legitimate in Australia?

Yes, reputable online business lenders operating in Australia are regulated and legitimate. Any lender offering credit products must hold an Australian Credit Licence (ACL) issued by ASIC, and must comply with the National Consumer Credit Protection Act where applicable.

That said, not all platforms are equal. Here's how to check:

- Verify the ACL number

- on ASIC's public register

- Check for AFCA membership

- the Australian Financial Complaints Authority handles disputes

- Read the credit contract carefully

- a legitimate lender will give you a written agreement before funds are released

- Avoid lenders who guarantee approval

- no legitimate lender can do this before assessing your application

Platforms that connect you with a panel of selected Australian finance partners add another layer of protection — the platform vets lenders before listing them, and you can compare offers without committing to any one of them. Understanding your rights is also covered in our article on what the Financial Services Act means for small business borrowers.

What Kinds of Businesses Should Avoid Online Lending Platforms?

Online lending isn't the right fit for every situation. Businesses that should lean toward a commercial banker include:

- Large borrowing needs above $2–3 million

- banks are more comfortable with these amounts and can structure complex facilities

- Long-term property or asset finance

- commercial mortgages and 10+ year equipment loans suit the bank model better

- Businesses with pristine financials and strong collateral

- if you qualify for a bank's best rate, the lower cost may outweigh the speed advantage of online lending

- Government-contracted businesses

- needing specific bank guarantees or performance bonds

Businesses that should lean toward online lenders:

- Hospitality venues needing fast cash for fit-outs or equipment

- Construction and trades firms bridging invoice gaps

- Retail and e-commerce operators managing seasonal inventory

- Any business that's been knocked back by a bank and needs an alternative fast

For a deeper look at the broker vs direct lender question, see our guide on business loan broker vs direct lender in Australia.

How Do Big Banks Like Commonwealth Compare to Fintech Lenders?

The big four Australian banks (Commonwealth, Westpac, ANZ, NAB) offer stability, competitive rates for qualified borrowers, and long-term relationship banking. Fintech lenders offer speed, flexibility, and access for businesses that don't meet bank criteria.

The preference gap is closing fast. Non-bank lenders are now preferred by 31% of SMEs, edging past the 28% who prefer traditional banks — a dramatic shift from a decade ago when fewer than 10% of SMEs planned to use non-bank lenders.

Head-to-head comparison:

| Factor | Big Four Banks | Online/Fintech Lenders |

|---|---|---|

| Approval rate (loans <$1M) | 25–35% | Significantly higher for 3+ yr businesses |

| Approval timeline | 21–35 days | 24–72 hours |

| Minimum credit score | ~680 | From ~550 |

| Collateral required | Usually yes | Often unsecured |

| Loan terms | 3–25 years | 3 months–5 years |

| Interest rate range | 6–12% APR | 10–40%+ |

| Repayment schedule | Monthly | Daily or weekly |

| Application process | Branch/portal, heavy docs | Online, bank feed, fast |

The right choice isn't about which institution is "better" — it's about which one fits your situation right now.

What Documents Do You Need to Apply for a Business Loan Online?

Most online lenders require far less paperwork than banks. The core documents are typically:

- 1

Bank statements

3 to 6 months of business account transactions (often pulled via secure bank feed)

- 2

ABN and ACN

to verify your business registration

- 3

Driver's licence

for identity verification of the business owner/director

- 4

Basic business details

trading name, industry, time in business, monthly revenue

Some lenders may also ask for:

- BAS statements (last 1–2 lodgements)

- ATO portal access or tax portal integration

- Accountant-prepared financials (for larger loans above $250k)

Banks require significantly more: 2–3 years of tax returns, audited financials, a business plan, asset and liability statements, and often a personal financial statement from all directors.

Our Australian Business Loan Approval Checklist walks through exactly what each lender type wants before they say yes.

Which Loan Type Is Better for Startups with Limited Financial History?

Startups face the hardest road with commercial banks. Most require at least 2–3 years of trading history and audited financials — which rules out any business under two years old almost automatically.

Online lenders are more accessible for early-stage businesses, but still have minimums. Most require:

- At least 6–12 months of trading

- A minimum monthly revenue (commonly $5,000–$10,000 per month)

- An active ABN

For businesses under 12 months old, the options narrow further. Government-backed grants and loans, revenue-based financing, or equity funding may be more realistic paths. Our guide on business loans for startups in Australia covers what's actually available when you have no track record.

What Are the Biggest Risks of Choosing an Online Lender Over a Traditional Bank?

The main risks are higher cost of capital, shorter repayment terms that strain cash flow, and the possibility of entering a debt cycle if the loan doesn't generate the revenue needed to repay it.

Specific risks to manage:

- Rate shock:

- A 25–35% effective rate on a short-term loan can erode margins quickly if the borrowed capital doesn't generate proportional return

- Daily repayments:

- Some online products deduct repayments daily from your business account — if revenue dips, this can create overdraft issues

- Rollover dependency:

- Repeatedly refinancing short-term loans to cover previous ones is a warning sign the product isn't right for your situation

- Predatory fringe lenders:

- A small number of unregulated operators exist — always verify the ACL before proceeding

The risk mitigation is straightforward: borrow only what you need, understand the total repayment amount before signing, and use a platform that matches you with vetted specialist partners rather than applying to random lenders directly.

Conclusion: Making the Right Call for Your Business in 2026

The Commercial Banker vs Online Business Lender debate doesn't have a universal winner — but for most Australian SMEs in 2026, the numbers tell a clear story. With bank approval rates sitting at 25–35% for loans under $1 million, timelines stretching past three weeks, and non-bank lending now the preferred choice for nearly one in three SMEs, the online lending market has earned its place as a genuine first option — not just a fallback.

The practical decision rule

- Go to a commercial banker if you need over $2 million, have 3+ years of clean financials, own real estate to offer as security, and can wait 3–5 weeks for a decision

- Go to an online lender if you need funds within days, your credit profile isn't perfect, you're unsecured, or you've already been knocked back by a bank

Business Funding. Made Simple. That's not just a tagline — it's the actual difference between waiting a month for a bank decision and being funded by Thursday.

The fastest way to find out what you qualify for is a 2 min check with no hard credit search and no obligation to proceed. Check Eligibility Now — it takes two minutes and won't affect your credit file.

Further reading

Frequently asked questions

What Exactly Does a Commercial Banker Do for Small Businesses?

A commercial banker is a relationship manager at a major or regional bank who assesses, structures, and manages business lending facilities. For Australian SMEs, this typically means term loans, overdrafts, trade finance, or commercial property lending — all assessed against the bank's internal credit policy.

How Much Faster Are Online Business Loans Compared to Traditional Bank Loans?

Online lenders are dramatically faster — typically 24 to 72 hours from application to funding, compared to 21 to 35 days for major Australian banks.

What Are the Average Interest Rates: Commercial Bank vs Online Lender in Australia?

Banks generally offer lower headline rates (6–12% APR) for borrowers who qualify, while online lenders charge 10–40% or more depending on the risk profile. The OECD reported that interest rates on outstanding Australian SME loans averaged 6.6% in 2024.

Can Small Businesses with Average Credit Still Get Approved Online?

Yes. Online lenders are built to assess businesses that don't fit the bank mould. While major banks typically require a credit score of 680 or above and 2–3 years of trading history, many online lenders will consider scores from 550 upward and businesses trading for as little as 6–12 months.

Which Type of Lender Typically Offers Lower Fees — and What Hidden Costs Should You Watch For?

Banks tend to have lower interest rates but more complex fee structures. Online lenders are more transparent upfront but may use factor rates or daily repayment schedules that make total cost harder to calculate at a glance.

Are Online Business Loans Safe and Legitimate in Australia?

Yes, reputable online business lenders operating in Australia are regulated and legitimate. Any lender offering credit products must hold an Australian Credit Licence (ACL) issued by ASIC, and must comply with the National Consumer Credit Protection Act where applicable.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.