How Much Money Can I Borrow to Start a Business: UK Startup Funding Guide

UK entrepreneurs can typically borrow £10,000 to £500,000 for startup funding, depending on their credit score, business plan strength, and chosen funding type. Unsecured business loans offer £10,000-£120,000 without collateral, while secured loans can reach £500,000+ but require assets as security.

Quick answer

UK entrepreneurs can typically borrow £10,000 to £500,000 for startup funding, depending on their credit score, business plan strength, and chosen funding type. Unsecured business loans offer £10,000-£120,000 without collateral, while secured loans can reach £500,000+ but require assets as security.

Key takeaways

- Most UK startups can access £10,000-£120,000 through unsecured business loans without risking personal assets

- Your borrowing limit depends on personal credit score, business plan quality, and monthly revenue projections

- Alternative funding like Merchant Cash Advances offers flexible criteria for businesses with inconsistent cash flow

- SBA-style government schemes provide cheaper rates but involve longer approval times and stricter requirements

- Bad credit doesn't eliminate options - specialist lenders offer funding with Flexible Criteria and higher rates

- Smart Tech platforms can provide Fast Decisions in minutes using Open Banking data instead of lengthy paperwork

- Most lenders require 6-12 months of trading history, but some offer pre-revenue startup funding

- Personal savings of 20-30% of total startup costs strengthens loan applications significantly

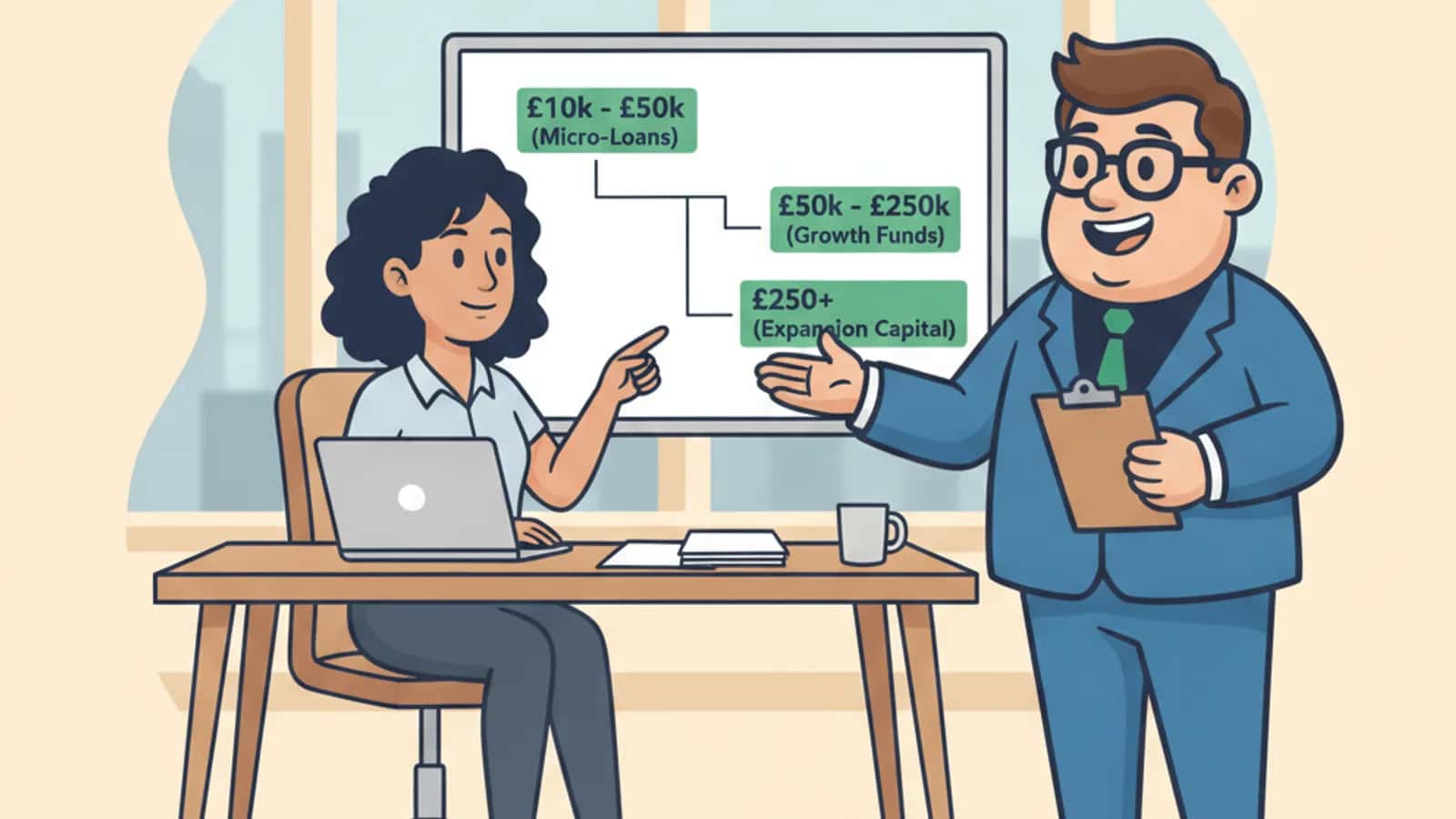

What Are the Typical Startup Loan Amounts for Small Businesses

UK startups typically access £10,000-£120,000 through unsecured business loans, while secured options can reach £500,000+ depending on collateral value. Most first-time entrepreneurs start with £25,000-£50,000 to cover initial setup costs and working capital.

Unsecured Business Loan Ranges

- Micro loans: £1,000-£10,000 for very small startups

- Standard business loans: £10,000-£50,000 for most new ventures

- Growth funding: £50,000-£120,000 for established concepts with strong projections

- Large unsecured: £120,000+ available but requires excellent credit and proven business model

Secured Loan Options

- Property-backed loans can reach £500,000-£2 million

- Asset finance covers 70-90% of equipment value

- Invoice finance provides up to 90% of outstanding invoices

The amount you can borrow depends heavily on your personal credit score, business sector, and projected monthly revenue. E-commerce stores often qualify for higher amounts due to scalable business models, while service businesses may face lower limits initially.

Choose unsecured funding if you want to protect personal assets and need Fast Decisions. Traditional secured loans work better for asset-heavy businesses like manufacturing or restaurants requiring substantial equipment investment.

How Hard Is It to Get a Business Loan with No Credit History

Getting a business loan with no credit history is challenging but not impossible - many UK lenders now use Open Banking technology and alternative data to assess creditworthiness beyond traditional credit scores. Expect higher interest rates and lower initial borrowing limits.

Alternative Assessment Methods

- Open Banking data shows spending patterns and cash flow management

- Bank statement analysis reveals financial discipline over 3-6 months

- Business plan strength can offset weak personal credit history

- Industry experience demonstrates ability to execute the venture

- Personal guarantees provide additional security for lenders

Realistic Expectations with No Credit

- Initial loans typically capped at £10,000-£25,000

- Interest rates 15-25% higher than prime borrowers

- Shorter repayment terms (12-24 months initially)

- More documentation required for approval

Specialist platforms using Smart Tech can provide decisions within minutes by analyzing real-time banking data instead of relying solely on credit bureau information. This approach particularly benefits young entrepreneurs or those new to the UK who lack extensive credit histories.

Can I Get Startup Funding If I Have Bad Personal Credit

Yes, you can secure startup funding with bad personal credit through specialist lenders who accept All Credit Types, though expect higher rates and additional requirements. Many UK platforms now offer Flexible Criteria lending specifically for entrepreneurs with credit challenges.

Bad Credit Funding Options

- Asset-based lending focuses on business assets rather than personal credit

- Merchant Cash Advances use future sales projections instead of credit scores

- Peer-to-peer lending connects you directly with individual investors

- Revenue-based financing ties repayments to actual business performance

Typical Terms with Poor Credit

- Interest rates: 20-45% APR depending on risk assessment

- Loan amounts: Usually capped at £15,000-£40,000 initially

- Repayment periods: Shorter terms (6-18 months) to reduce lender risk

- Additional security: May require personal guarantees or business assets

The key is demonstrating strong business fundamentals despite personal credit issues. A solid business plan, industry experience, and realistic financial projections can outweigh past credit problems for many alternative lenders.

What's the Difference Between Government Schemes and Traditional Bank Loans

Government-backed schemes like the Recovery Loan Scheme offer lower rates (6-12% APR) and 70-80% government guarantees but involve longer approval times and stricter criteria. Traditional bank loans provide faster decisions but require stronger credit profiles and often demand personal guarantees.

Government Scheme Advantages

- Lower interest rates due to government backing

- Higher approval rates for marginal applications

- Longer repayment terms up to 6 years

- Less personal liability with government guarantee coverage

Traditional Bank Loan Benefits

- Faster approval typically 2-4 weeks vs 6-12 weeks

- Simpler application process with less documentation

- Relationship building for future funding needs

- Flexible terms can be negotiated based on circumstances

Alternative Platform Advantages

- Instant decisions using Smart Tech and Open Banking

- No hard check to start the application process

- Wide partner panel increases approval chances

- Flexible repayment options matching cash flow patterns

Choose government schemes if you have time to wait and want the lowest possible rates. Pick traditional banks for established businesses with strong credit. Select alternative platforms when you need Fast Decisions and have Flexible Criteria requirements.

How Much Money Do I Really Need to Launch My Type of Business

Startup capital requirements vary dramatically by business type, from £5,000 for online services to £200,000+ for restaurants or manufacturing. Most UK entrepreneurs underestimate working capital needs by 30-50%, making realistic financial planning crucial.

Typical Startup Costs by Sector:

Essential Cost Categories

- Setup costs: Equipment, licenses, initial inventory

- Operating expenses: Rent, utilities, insurance for 6-12 months

- Marketing budget: 10-15% of first-year revenue projections

- Emergency buffer: 20-30% contingency for unexpected expenses

Working capital often determines success more than initial setup costs. A restaurant might spend £100,000 on fit-out but fail without £30,000 working capital to cover slow initial months.

What Are the Cheapest Ways to Get Initial Business Funding

The cheapest startup funding comes from personal savings, family loans, and government grants, with costs ranging from 0-6% compared to 15-35% for commercial lending. However, speed and availability often make higher-cost options more practical for time-sensitive opportunities.

Funding Options by Cost:

Free/Low Cost (0-6%)

- Personal savings and family loans

- Government grants and competitions

- Crowdfunding platforms

- Business partner investment

Moderate Cost (8-15%)

- Government-backed loan schemes

- Traditional bank loans with good credit

- Credit unions and community lenders

Higher Cost but Fast (15-35%)

- Unsecured business loans

- Merchant Cash Advances

- Asset-based lending

- Revenue-based financing

Cost vs Speed Trade-off: Traditional banks offer rates around 8-12% but take 4-8 weeks for approval. Alternative lenders provide Fast Decisions within 24 hours but charge 18-25% APR. The extra cost often pays for itself if it means capturing time-sensitive opportunities.

Do I Qualify for a Business Loan as a First-Time Entrepreneur

First-time entrepreneurs can qualify for business loans, but most lenders prefer 6-12 months of trading history or strong personal credit scores above 650. Alternative lenders using Flexible Criteria focus more on business plan strength and industry experience than entrepreneurial track record.

Qualification Factors for New Entrepreneurs

- Personal credit score: 650+ significantly improves approval chances

- Industry experience: Previous employment in the target sector

- Business plan quality: Detailed financial projections and market analysis

- Personal investment: 20-30% of total funding from own resources

- Guarantees available: Personal or business assets for security

First-Timer Friendly Options

- Start-up loans specifically designed for new entrepreneurs

- Mentor-backed programs combining funding with business support

- Industry-specific schemes for sectors like technology or green energy

- Alternative platforms using Smart Tech for rapid assessment

Typical First-Time Limits

- Unsecured loans: £10,000-£40,000 initially

- Secured options: Up to asset value with personal guarantees

- Revenue-based: 10-20% of projected annual revenue

The key is demonstrating competence despite lack of business ownership history. Previous management experience, relevant qualifications, and a well-researched business plan can substitute for entrepreneurial track record.

What Credit Score Do I Need to Borrow Money for a Startup

Most UK lenders prefer credit scores above 650 for competitive rates, though scores of 550-649 can still access funding with higher interest rates and additional requirements. Specialist lenders accept scores below 550 using alternative assessment methods and Flexible Criteria.

Credit Score Lending Tiers:

Excellent (750+)

- Access to best rates (8-15% APR)

- Higher borrowing limits up to £120,000+

- Minimal documentation required

- Fast approval processes

Good (650-749)

- Standard rates (12-20% APR)

- Moderate limits £25,000-£75,000

- Normal application requirements

- Good approval chances

Fair (550-649)

- Higher rates (18-28% APR)

- Lower limits £10,000-£40,000

- Additional documentation needed

- Specialist lender territory

Poor (Below 550)

- Premium rates (25-40% APR)

- Minimal limits £5,000-£20,000

- Secured options preferred

- Alternative assessment methods

Beyond Credit Scores: Modern lenders increasingly use Open Banking data, business plan analysis, and industry experience alongside credit scores. A score of 580 with strong banking behavior and solid business fundamentals often outperforms a 720 score with poor cash flow management.

Improvement tip: Use "No hard check to start" applications to understand your options without damaging your credit score further. Many platforms provide soft credit checks that don't affect your rating.

Are There Grants or Alternative Funding Sources for New Businesses

UK entrepreneurs can access numerous grants and alternative funding sources, from government innovation grants worth £25,000-£100,000+ to crowdfunding and angel investment networks. However, grants often have strict eligibility criteria and lengthy application processes compared to commercial lending.

Government Grant Options

- Innovate UK grants: £25,000-£2 million for innovative businesses

- Local Enterprise Partnership funds: £5,000-£50,000 regional support

- Sector-specific schemes: Green energy, technology, manufacturing focus

- Start-up loan scheme: £500-£25,000 with mentoring support

Alternative Funding Sources

- Angel investors: £10,000-£500,000 for high-growth potential

- Crowdfunding platforms: £1,000-£100,000+ from public backing

- Revenue-based financing: Funding tied to future sales performance

- Equipment finance: 70-90% of asset value for machinery/vehicles

Pros and Cons Comparison:

Grants

- No repayment required

- Often include business support

- Highly competitive application process

- Lengthy approval times (3-12 months)

Commercial Lending

- Fast Decision capability

- Predictable approval criteria

- Interest and repayment obligations

- Available when opportunities arise

What Mistakes Do Most Entrepreneurs Make When Seeking Startup Capital

The biggest mistake entrepreneurs make is underestimating working capital needs by 30-50%, focusing only on setup costs while ignoring months of operating expenses before reaching profitability. Many also damage their credit scores by applying to multiple traditional lenders instead of using Smart Tech platforms with soft credit checks.

Common Funding Mistakes:

Financial Planning Errors

- Underestimating costs by excluding working capital requirements

- Overestimating revenue in early months leading to cash flow gaps

- Ignoring seasonality in business projections and cash needs

- Missing contingency planning for 20-30% cost overruns

Application Strategy Mistakes

- Wrong lender targeting - applying to traditional banks with poor credit

- Multiple hard credit checks damaging credit scores unnecessarily

- Incomplete documentation causing delays and rejections

- Unrealistic loan amounts requesting more than business justifies

Timing and Process Errors

- Last-minute applications when cash flow crisis already started

- Single funding source dependency without backup options

- Ignoring alternative options like Merchant Cash Advances for flexible repayment

- Poor presentation of business plans and financial projections

Edge case awareness: Some funding types exclude specific industries or business models. Research eligibility criteria before investing time in lengthy applications.

How Much Personal Savings Should I Have Before Applying

Most successful business loan applications include 20-30% personal investment of the total startup costs, demonstrating commitment and reducing lender risk. Having £10,000-£15,000 in personal savings significantly improves approval chances even for larger loan amounts.

Personal Investment Guidelines

- Minimum recommended: 15-20% of total startup costs from personal funds

- Optimal level: 25-35% personal investment for best rates and terms

- Emergency reserve: Additional 3-6 months personal living expenses separate from business investment

- Working capital contribution: Personal funds should cover at least initial operating costs

Why Personal Investment Matters

- Risk sharing shows commitment to lenders

- Lower loan amounts needed reduces monthly repayments

- Better terms available with substantial personal contribution

- Flexibility buffer for unexpected costs or delays

Savings Strategy by Business Type:

Alternative approach: If personal savings are limited, consider revenue-based financing or Merchant Cash Advances that focus on business potential rather than upfront investment levels. These options typically require smaller personal contributions but carry higher costs.

What Documentation Do I Need to Apply for a Small Business Loan

UK business loan applications typically require 3-6 months of bank statements, a detailed business plan with financial projections, and proof of identity, though Smart Tech platforms using Open Banking can streamline this to basic identity verification and account connections.

Essential Documentation

- Personal identification: Passport or driving license plus proof of address

- Business plan: Executive summary, market analysis, financial projections

- Bank statements: 3-6 months personal and business accounts if available

- Financial projections: Monthly cash flow forecasts for 12-24 months

- Industry experience: CV or evidence of relevant background

Traditional Bank Requirements

- Detailed business plan (20-40 pages)

- Comprehensive financial forecasts with sensitivity analysis

- Personal financial statements including assets and liabilities

- Security documentation for secured lending options

- Professional references and credit checks

Modern Platform Requirements

- Basic business plan (5-10 pages)

- Open Banking connection for automatic bank statement analysis

- Simple financial projections using provided templates

- Identity verification through digital processes

- No hard check to start preliminary assessments

Document Preparation Tips

- Conservative projections: Better to under-promise and over-deliver

- Professional presentation: Use business plan templates and clear formatting

- Supporting evidence: Include market research and competitor analysis

- Regular updates: Keep financial projections current with market conditions

Time-saving approach: Start with platforms offering 2 min check processes using Open Banking. These provide instant feedback on likely approval amounts before investing time in comprehensive documentation for traditional lenders.

Next steps for how much money can i borrow to start a business

Understanding how much money you can borrow to start a business depends on balancing your funding needs with available options that match your credit profile and timeline requirements. UK entrepreneurs typically access £10,000-£120,000 through various funding sources, from traditional bank loans requiring excellent credit to alternative platforms offering Flexible Criteria and Fast Decisions.

The key to successful startup funding lies in realistic financial planning - including adequate working capital alongside setup costs - and choosing the right funding mix for your situation. While government schemes offer the lowest rates, alternative lenders provide speed and accessibility that often justify higher costs for time-sensitive opportunities.

Ready to explore your funding options? Check Eligibility Now through platforms offering No hard check to start assessments. Use Open Banking connections to get instant feedback on borrowing potential, then compare offers from Wide partner panels to find the best terms for your startup's specific needs.

Start with conservative loan amounts that match realistic revenue projections, maintain strong personal financial discipline, and keep comprehensive documentation ready for quick application processes. Success often comes from having multiple funding options prepared rather than relying on a single source.

Further reading

Frequently asked questions

What Are the Typical Startup Loan Amounts for Small Businesses?

UK startups typically access £10,000-£120,000 through unsecured business loans, while secured options can reach £500,000+ depending on collateral value. Most first-time entrepreneurs start with £25,000-£50,000 to cover initial setup costs and working capital.

How Hard Is It to Get a Business Loan with No Credit History?

Getting a business loan with no credit history is challenging but not impossible - many UK lenders now use Open Banking technology and alternative data to assess creditworthiness beyond traditional credit scores. Expect higher interest rates and lower initial borrowing limits.

Can I Get Startup Funding If I Have Bad Personal Credit?

Yes, you can secure startup funding with bad personal credit through specialist lenders who accept All Credit Types, though expect higher rates and additional requirements. Many UK platforms now offer Flexible Criteria lending specifically for entrepreneurs with credit challenges.

What's the Difference Between Government Schemes and Traditional Bank Loans?

Government-backed schemes like the Recovery Loan Scheme offer lower rates (6-12% APR) and 70-80% government guarantees but involve longer approval times and stricter criteria. Traditional bank loans provide faster decisions but require stronger credit profiles and often demand personal guarantees.

How Much Money Do I Really Need to Launch My Type of Business?

Startup capital requirements vary dramatically by business type, from £5,000 for online services to £200,000+ for restaurants or manufacturing. Most UK entrepreneurs underestimate working capital needs by 30-50%, making realistic financial planning crucial.

What Are the Cheapest Ways to Get Initial Business Funding?

The cheapest startup funding comes from personal savings, family loans, and government grants, with costs ranging from 0-6% compared to 15-35% for commercial lending. However, speed and availability often make higher-cost options more practical for time-sensitive opportunities.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Reviewed by

UK business finance content reviewer

Robert reads our UK business finance guides before they go live, checking each one is accurate, easy to follow, and reflects how lending actually works today — not how a brochure says it should. He's listed on the FCA Register, approved as an SMF3 (AR) Executive Director at Switcha Limited, and connected to Lucky Growth Partners Ltd through its appointed representative relationship, so the regulated detail gets a properly qualified second read.