Invoice Finance for Agencies and Consultancies: Funding Project Work on 30-90 Day Terms

Invoice finance for agencies and consultancies converts unpaid client invoices into immediate cash flow, typically advancing 80-95% of invoice value within 24 hours.

Quick answer

Invoice finance for agencies and consultancies converts unpaid client invoices into immediate cash flow, typically advancing 80-95% of invoice value within 24 hours. This funding solution addresses the common challenge of waiting 30-90 days for client payments while covering payroll, supplier costs, and new project expenses without taking on traditional debt.

Key takeaways

- Invoice finance provides same-day funding against outstanding client invoices, with advances of 80-95% of invoice value

- Agencies can access funding from £10,000 to £5 million+ through specialist invoice finance partners

- Two main types available: invoice factoring (provider manages collections) and invoice discounting (you retain control)

- Costs typically range from 1-5% of invoice value, often cheaper than business overdrafts or emergency loans

- No personal guarantees required with many providers, unlike traditional business loans

- Eligibility focuses on client creditworthiness rather than agency credit history

- Funding decisions made within hours, not weeks like conventional lending

- Selective invoice financing allows agencies to choose which invoices to finance and when

- Works best for B2B agencies with invoices over £1,000 and payment terms of 30+ days

- Risk protection available through non-recourse factoring if clients fail to pay

What Exactly Is Invoice Finance and How Does It Work for Creative Agencies

Invoice finance transforms unpaid client invoices into immediate working capital by selling your outstanding receivables to a specialist finance provider. For creative agencies, this means getting paid within 24 hours instead of waiting 30-90 days for clients to settle their bills.

The process works in three simple steps. First, you complete your project work and issue invoices to clients as normal. Second, you submit approved invoices to your invoice finance provider, who advances 80-95% of the invoice value immediately. Third, when your client pays, the provider releases the remaining balance minus their fee.

Two Main Types for Agencies:

Invoice Factoring - The finance provider takes over credit control and collections. Your clients pay the factoring company directly. This option works well for agencies wanting to outsource debt collection entirely.

Invoice Discounting - You retain control of client relationships and collections. Clients continue paying you directly, then you repay the advance plus fees. This maintains confidentiality and preserves client relationships.

Creative agencies particularly benefit because project-based work often involves large upfront costs for staff, freelancers, and suppliers, but payment arrives weeks or months later. Invoice finance bridges this gap without the lengthy approval process of traditional business loans.

The funding is tied directly to your sales ledger rather than your credit history, making it accessible for growing agencies with strong client bases but limited trading history.

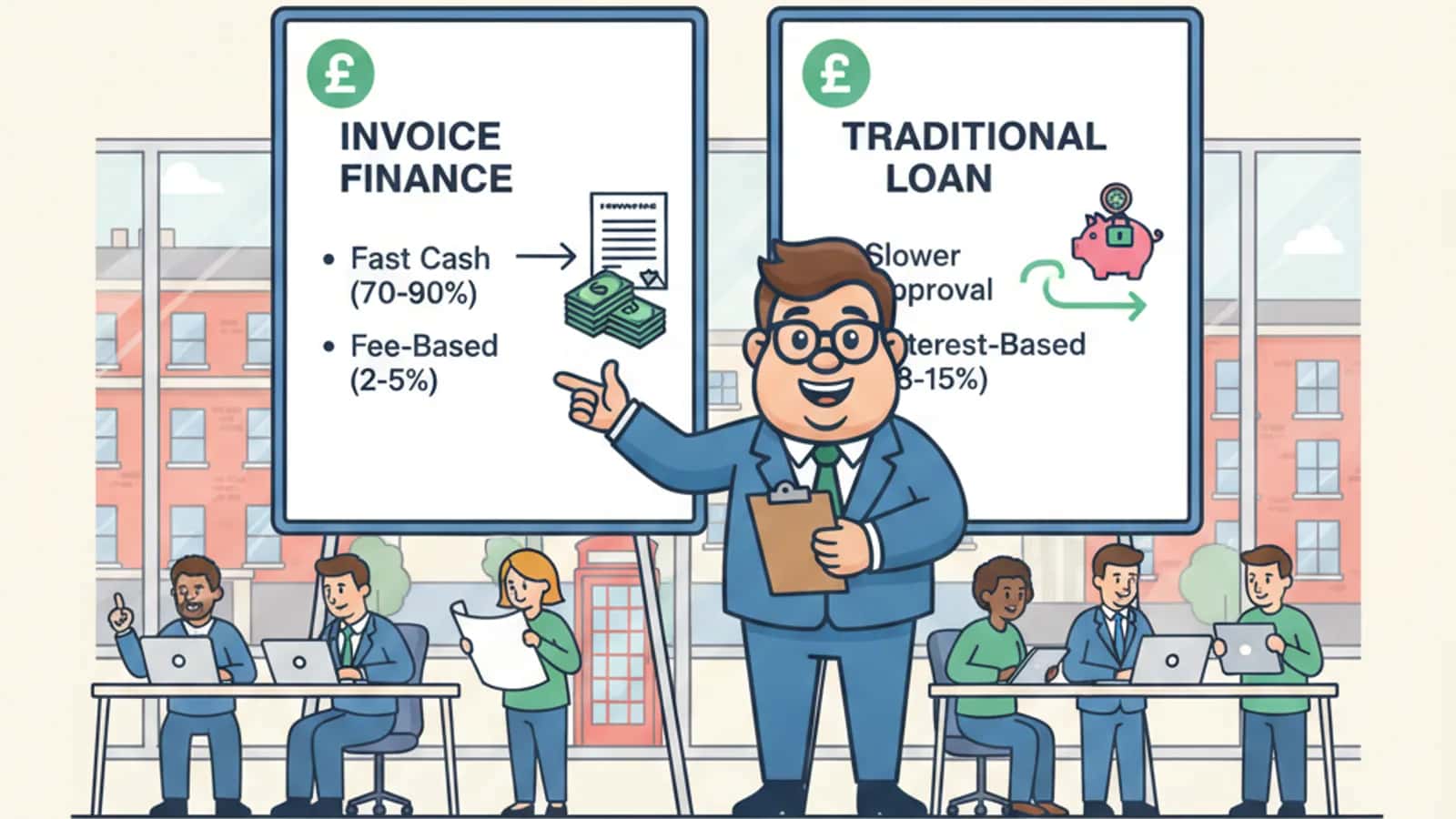

How Much Does Invoice Financing Cost Compared to Traditional Business Loans

Invoice financing typically costs 1-5% of the invoice value, which often works out cheaper than business overdrafts or emergency funding when you factor in speed and flexibility. Unlike traditional loans with fixed monthly payments, you only pay fees on invoices you actually finance.

Typical Cost Structure

- Discount fee: 1-3% of invoice value (one-time charge)

- Service fee: 0.5-2% per month on outstanding balances

- Total cost: Usually 2-5% of invoice value for 30-60 day payment terms

Compare this to business loan alternatives. A £50,000 business loan at 8% APR costs approximately £333 monthly in interest alone. Invoice financing a £50,000 invoice at 3% total cost equals £1,500 - but you get the money in 24 hours and only pay when you use it.

The key advantage is flexibility. With invoice financing, you control when to access funding and only pay for what you use. Traditional loans require fixed monthly payments regardless of cash flow needs.

For agencies with seasonal work or project-based income, this pay-as-you-go model often proves more cost-effective than maintaining expensive overdraft facilities or loan commitments year-round.

Can Small Design Consultancies Qualify for Invoice Factoring

Small design consultancies can qualify for invoice factoring with monthly invoicing as low as £10,000, making it accessible for boutique agencies and growing consultancies. Approval focuses on client creditworthiness rather than consultancy size or trading history.

Minimum Requirements

- Monthly invoicing of £10,000-£25,000 depending on provider

- B2B clients with good payment history

- Invoice values typically £1,000+ per invoice

- UK-registered business with business bank account

- Invoices with payment terms of 30+ days

Small consultancies often find invoice factoring easier to access than traditional business finance because the decision is based on their clients' ability to pay, not the consultancy's credit score or asset base. A two-person design agency working with established corporate clients can access the same funding rates as larger agencies.

Advantages for Small Consultancies

- No personal guarantees required with many providers

- Credit decisions made within hours, not weeks

- Funding grows automatically as client base expands

- Professional collections service included with factoring

- Improved cash flow enables taking on larger projects

The key is having creditworthy B2B clients. A small consultancy working with established businesses, government departments, or larger agencies will find approval straightforward. However, consultancies primarily serving startups or individuals may face more limited options.

Many providers offer selective invoice financing, allowing small consultancies to finance only their larger invoices or those from slower-paying clients while maintaining normal payment terms with others.

What Are the Risks of Using Invoice Financing for Marketing Agencies

The main risks of invoice financing for marketing agencies include client relationship impacts, cost accumulation on slow-paying invoices, and potential disputes over work quality affecting payment. However, these risks are manageable with proper provider selection and clear client contracts.

Primary Risk Areas:

Client Relationship Risk

- With invoice factoring, clients pay the finance provider directly, potentially raising questions about your financial stability. Choose providers with professional collections processes and consider invoice discounting to maintain direct client relationships.

Cost Escalation

- Fees continue accumulating until clients pay, making chronically slow payers expensive to finance. Set clear payment terms and consider factoring only with clients who typically pay within 60 days.

Dispute Risk

- If clients dispute work quality or deliverables, they may withhold payment while you still owe the advance to the finance provider. Maintain detailed project documentation and clear approval processes to minimize disputes.

Concentration Risk

- Over-reliance on financing invoices from a few large clients creates vulnerability if those relationships end. Diversify your client base and avoid financing more than 50% of revenue from any single client.

Recourse vs Non-Recourse

- With recourse factoring, you remain liable if clients don't pay. Non-recourse factoring provides protection against bad debts but costs more and has stricter client approval requirements.

Mitigation Strategies

- Use invoice discounting to maintain client confidentiality

- Finance selectively rather than all invoices

- Maintain strong project documentation and approval processes

- Choose providers with professional collections approaches

- Consider non-recourse options for higher-risk clients

Most marketing agencies find the benefits outweigh the risks when invoice finance is used strategically rather than as a blanket solution for all receivables.

Which Invoice Finance Providers Work Best for Digital Agencies Under 50 Employees

Specialist invoice finance providers focusing on professional services and creative industries typically work best for digital agencies under 50 employees, offering flexible terms and understanding of project-based cash flow challenges.

Key Provider Characteristics

- Experience with creative and digital sectors

- Flexible selective invoice financing options

- Competitive rates for smaller invoice volumes

- Fast approval and funding processes

- Professional collections approach that preserves client relationships

Digital agencies should prioritize providers offering selective invoice financing, allowing them to choose which invoices to finance based on client payment history and cash flow needs. This flexibility is crucial for agencies with mixed client bases including both prompt payers and slower corporate clients.

Evaluation Criteria

- Minimum requirements: Look for providers accepting £10,000+ monthly invoicing rather than £100,000+ minimums

- Advance rates: Seek 85-95% advance rates on approved invoices

- Speed: Prioritize same-day funding capability for urgent cash flow needs

- Technology: Choose providers with online portals for easy invoice submission and tracking

- Sector knowledge: Select providers familiar with digital marketing, web development, and creative services

Many digital agencies benefit from starting with a 2-minute eligibility check to compare options without impacting credit scores. This approach helps identify specialist partners who understand the unique cash flow patterns of project-based businesses.

Avoid providers who

- Require personal guarantees or security

- Insist on financing all invoices rather than selective options

- Have lengthy approval processes exceeding 48 hours

- Lack experience with professional services sectors

The best providers for smaller digital agencies combine competitive pricing with flexibility and speed, recognizing that these businesses need funding solutions that adapt to project-based revenue patterns.

How Quickly Can Agencies Get Cash Advances Against Outstanding Client Invoices

Agencies can typically receive cash advances against outstanding invoices within 24 hours of approval, with some providers offering same-day funding for urgent cash flow needs. The speed depends on having pre-approved client lists and streamlined submission processes.

Typical Timeline:

- 1

Application

2-10 minutes online

- 2

Initial approval

2-4 hours during business hours

- 3

Client verification

24-48 hours for new clients

- 4

Funding

Same day or next business day after approval

- 5

Ongoing invoices

Instant funding for pre-approved clients

Factors Affecting Speed

- Pre-approved clients: Invoices from previously verified clients fund immediately

- New client verification: First-time clients require credit checks, adding 24-48 hours

- Invoice documentation: Complete, clear invoices process faster than incomplete submissions

- Submission timing: Applications before 2 PM typically fund same day

The fastest funding comes from providers offering selective invoice financing with pre-approved client databases. Once your regular clients are verified, submitting invoices becomes a simple online process with funding arriving within hours.

Speed Optimization Tips

- Complete provider onboarding fully before needing urgent funding

- Submit clear, complete invoices with all supporting documentation

- Maintain updated client contact information in the provider's system

- Use providers with 24/7 online submission portals

- Apply early in the business day for same-day funding

For agencies needing same-day business funding, invoice finance often proves faster than business loans, overdrafts, or other traditional funding sources that require lengthy approval processes and credit committee decisions.

The key is preparation. Agencies that set up invoice finance facilities before needing urgent funding can access cash within hours when cash flow challenges arise.

What Happens If a Client Doesn't Pay After Getting Invoice Financing

If a client doesn't pay after you've received invoice financing, the outcome depends on whether you chose recourse or non-recourse factoring, with different levels of protection and responsibility for bad debts.

Recourse Factoring (Standard Option): With recourse factoring, you remain ultimately responsible for unpaid invoices. If a client doesn't pay within the agreed timeframe (typically 90-120 days), you must repay the advance plus fees to the finance provider. This option costs less but leaves you liable for bad debts.

Non-Recourse Factoring (Protected Option): Non-recourse factoring protects you against bad debts from approved clients. If a client becomes insolvent or fails to pay for reasons beyond your control, the finance provider absorbs the loss. This protection costs more (typically 0.5-1% extra) but provides valuable security.

Typical Process for Non-Payment:

- Days 1-30: Normal payment period

- Days 31-60: Provider begins collection efforts

- Days 61-90: Escalated collections, potential legal action

- Days 91+: Bad debt procedures activated based on agreement type

Your Options When Clients Don't Pay

- Negotiate payment plans with clients while keeping the provider informed

- Provide additional documentation to support collection efforts

- Replace the invoice with a paid invoice if using recourse factoring

- Claim bad debt protection if using non-recourse and criteria are met

Prevention Strategies

- Choose clients with strong payment histories for financing

- Maintain detailed project documentation and approval records

- Use non-recourse factoring for higher-risk or new clients

- Monitor client payment patterns and adjust financing decisions accordingly

Most providers offer comprehensive support services including credit research and professional collections to minimize bad debt risks while preserving client relationships.

Invoice Finance Options Without Personal Guarantees

Many invoice finance providers offer facilities without personal guarantees, basing approval on client creditworthiness rather than director guarantees or business assets. This makes invoice finance more accessible than traditional business loans for agency owners.

Why Personal Guarantees Aren't Required: Invoice finance is secured against your sales ledger rather than personal assets. The finance provider's primary concern is your clients' ability to pay, not your personal financial position. This fundamental difference makes it a lower-risk option for business owners.

Providers Offering No Personal Guarantee Options

- Specialist invoice finance companies focusing on professional services

- Selective invoice financing providers who assess each client individually

- Non-recourse factoring providers who take on collection risks

- Technology-focused providers using automated credit assessment systems

Alternative Security Requirements: Instead of personal guarantees, providers typically require:

- Client credit checks

- and approval processes

- Invoice verification

- and authenticity confirmation

- Business bank account

- access for payment monitoring

- Professional indemnity insurance

- for service-based businesses

- Clear contract terms

- with clients including payment schedules

Benefits for Agency Owners

- Personal asset protection - Your home and personal savings remain separate

- Easier approval process - Focus on business performance rather than personal credit

- Faster decisions - Automated client credit assessment speeds approval

- Scalable funding - Credit limits based on client quality, not personal wealth

When Personal Guarantees May Be Required

- Very new businesses with limited trading history

- Agencies with poor client payment records

- High-risk sectors or client bases

- Large funding requirements exceeding standard risk parameters

For most established agencies with creditworthy B2B clients, invoice finance without personal guarantees provides a viable alternative to traditional lending while protecting personal assets from business risks.

Common Mistakes Agencies Make When Using Invoice Financing

The most common mistake agencies make is financing all invoices regardless of client payment history, leading to unnecessary costs and potential cash flow complications. Successful agencies use invoice finance selectively and strategically.

Major Mistakes to Avoid:

Financing Fast-Paying Clients

- Don't finance invoices from clients who typically pay within 14-21 days. The cost often exceeds the benefit, and you're paying for funding you don't need. Reserve financing for clients with 45+ day payment cycles.

Ignoring Cost Accumulation

- Fees continue building until clients pay, making chronically slow payers expensive to finance. Set internal rules about maximum financing periods and consider alternative collection methods for persistent late payers.

Poor Invoice Documentation

- Submitting incomplete or unclear invoices delays funding and creates disputes. Ensure all invoices include detailed work descriptions, clear payment terms, and proper client approval documentation.

Over-Reliance on Single Clients

- Financing too much revenue from one client creates concentration risk. If that client relationship ends or payment issues arise, your entire cash flow suffers. Diversify both clients and financing decisions.

Choosing Wrong Provider Type

- Using invoice factoring when client confidentiality matters, or selecting providers without sector experience. Match the provider type to your business needs and client relationship requirements.

Neglecting Client Communication

- With invoice factoring, clients interact with your finance provider. Poor communication about this change can damage relationships. Introduce the process professionally and explain the benefits.

Strategic Best Practices

- Finance selectively based on client payment history and cash flow needs

- Maintain direct client relationships where possible using invoice discounting

- Monitor costs carefully and set maximum financing periods

- Use financing to enable growth, not cover operational shortfalls

- Keep detailed records of financed vs. non-financed invoice performance

Red Flag Situations

- Financing more than 70% of total revenue

- Using invoice finance to cover losses rather than timing gaps

- Financing disputed or potentially disputed invoices

- Ignoring client credit deterioration signals

Success with invoice finance comes from treating it as a strategic cash flow tool rather than a general funding solution for all receivables.

How Invoice Financing Differs from Business Lines of Credit

Invoice financing provides funding secured against specific unpaid invoices, while business lines of credit offer general-purpose borrowing secured against business assets or guarantees. The key difference lies in security, approval criteria, and usage flexibility.

Security and Approval Differences:

Invoice Financing

- Secured against your sales ledger and client creditworthiness

- Approval based on client payment history and invoice quality

- No personal guarantees required in most cases

- Credit decisions made within hours based on client verification

Business Lines of Credit

- Secured against business assets, property, or personal guarantees

- Approval based on business credit history, profitability, and director creditworthiness

- Often requires personal guarantees and business asset security

- Credit decisions take days or weeks with full financial assessment

Usage and Cost Comparison:

| Factor | Invoice Financing | Business Line of Credit |

|---|---|---|

| Funding Speed | 24 hours | 1-4 weeks |

| Security Required | Sales ledger | Assets/guarantees |

| Cost Structure | Pay per invoice (1-5%) | Interest on drawn amounts (5-15% APR) |

| Credit Limit | Based on invoice values | Fixed limit based on assets |

| Usage Flexibility | Invoice-specific | General business purposes |

| Repayment | When clients pay | Flexible repayment terms |

Which is right for you?

When to Choose Invoice Financing

- You have creditworthy B2B clients with extended payment terms

- Need funding tied to specific projects or invoices

- Want to avoid personal guarantees or asset security

- Require fast access to working capital

- Have seasonal or project-based cash flow patterns

When to Choose Lines of Credit

- Need general-purpose business funding for various expenses

- Want ongoing access to funds regardless of invoice levels

- Have strong business assets to secure favorable rates

- Require funding for inventory, equipment, or expansion rather than cash flow timing

Many agencies benefit from combining both solutions - using invoice financing for immediate cash flow needs and maintaining a smaller line of credit for general business expenses and opportunities.

Is Invoice Finance Suitable for Agencies with Inconsistent Project Revenue

Invoice finance works well for agencies with inconsistent project revenue because funding scales automatically with invoice values and you only pay fees on invoices you actually finance. This flexibility makes it more suitable than fixed-cost funding for variable income patterns.

Advantages for Variable Revenue Agencies:

Scalable Funding

- Credit limits adjust based on your outstanding invoices rather than fixed amounts. During busy periods with large projects, more funding becomes available automatically. During quiet periods, you're not paying for unused credit facilities.

Pay-As-You-Go Costs

- Unlike business loans with fixed monthly payments, invoice finance costs only apply to invoices you choose to finance. This matches your cost structure to your actual funding needs and revenue patterns.

Selective Usage

- Finance only large invoices or those from slow-paying clients while maintaining normal payment cycles with regular clients. This strategic approach minimizes costs while maximizing cash flow benefits.

Project-Based Matching

- Large projects often require significant upfront costs for staff, freelancers, and suppliers before invoicing. Invoice finance bridges this gap without the ongoing commitment of traditional lending.

Seasonal Flexibility

- Many agencies experience seasonal revenue variations. Invoice finance provides funding during peak periods without the burden of unused credit facilities during quieter months.

Managing Inconsistent Revenue

- Set minimum thresholds - Only finance invoices above certain values to ensure cost-effectiveness

- Monitor client payment patterns - Focus financing on clients with predictable but extended payment cycles

- Plan for quiet periods - Use invoice finance strategically to build cash reserves during busy periods

- Diversify client base - Reduce revenue volatility by spreading work across multiple clients and sectors

Best Practices for Variable Income

- Maintain detailed cash flow forecasts to predict financing needs

- Use selective invoice financing rather than blanket facilities

- Build relationships with multiple providers for different funding requirements

- Keep some invoices unfinanced to maintain direct client payment relationships

For agencies with inconsistent project revenue, invoice finance often proves more cost-effective and flexible than maintaining expensive overdraft facilities or loan commitments during periods of variable income.

Documentation Required for Invoice Finance Applications

Invoice finance applications require basic business documentation plus details about your clients and invoicing processes, with most providers accepting digital submissions for faster processing. The documentation focuses on verifying your business legitimacy and client creditworthiness rather than extensive financial history.

Essential Business Documents

- Certificate of incorporation or business registration documents

- Business bank statements for the last 3-6 months

- VAT registration certificate if applicable

- Professional indemnity insurance certificate for service businesses

- Sample client contracts showing standard payment terms

Client and Invoice Information

- Client contact details including registered addresses and key contacts

- Sample invoices showing your standard invoicing format and terms

- Aged debtor reports or sales ledger summaries

- Client payment history demonstrating typical payment patterns

- Details of largest clients including company information and trading history

Financial Information (Minimal)

- Recent management accounts or basic profit and loss statements

- Details of existing credit facilities including overdrafts or loans

- Director identification including proof of address and identity

Ongoing Submission Requirements: Once approved, ongoing submissions typically require:

- Copy invoices

- for financing (usually submitted electronically)

- Proof of delivery

- or work completion where applicable

- Client purchase orders

- or project approval documentation

- Monthly aged debtor reports

- to track payment progress

Digital Submission Process: Most modern providers offer online portals allowing:

- Instant invoice uploads

- via smartphone apps or web portals

- Automated client verification

- for repeat customers

- Real-time funding status

- tracking and notifications

- Digital document storage

- eliminating paperwork requirements

Speed Optimization

- Prepare documents in advance before needing urgent funding

- Use clear, professional invoice formats to speed verification

- Maintain updated client information in provider systems

- Submit complete applications to avoid delays from missing information

The documentation requirements are typically less onerous than traditional business loans, focusing on operational verification rather than extensive financial analysis. Most applications can be completed online within 10-15 minutes once you have the basic documents prepared.

Can Freelancers and Solopreneurs Use Invoice Finance

Freelancers and solopreneurs can use invoice finance if they operate as limited companies and invoice business clients, though minimum requirements may limit access for very small-scale operations. The key is having B2B invoices of sufficient value and creditworthy clients.

Eligibility for Solo Operators:

Minimum Requirements

- Limited company status - Most providers require incorporation rather than sole trader status

- Monthly invoicing of £5,000-£10,000 minimum depending on provider

- Individual invoice values typically £500-£1,000 minimum

- B2B clients - Consumer/B2C invoices rarely accepted

- Payment terms of 30+ days to justify financing costs

Suitable Freelancer Types

- IT contractors working on corporate projects

- Marketing consultants serving business clients

- Design professionals with agency or corporate clients

- Technical writers producing content for businesses

- Business consultants working on extended projects

Challenges for Solopreneurs

- Minimum volume requirements may exclude very small operations

- Cost-effectiveness - Small invoices may not justify financing fees

- Client concentration - Relying on 1-2 clients creates risk

- Administrative overhead - Managing financing relationships requires time

Alternative Solutions: For freelancers not meeting invoice finance minimums:

- Faster payment incentives

- Offer small discounts for early payment

- Milestone payments

- Structure projects with regular payment points

- Retainer arrangements

- Secure upfront payments for ongoing work

- Working capital solutions

- designed for smaller businesses

Making Invoice Finance Work as a Freelancer

- Group invoices strategically to meet minimum values

- Focus on larger corporate clients with established credit histories

- Maintain diverse client base to reduce concentration risk

- Use selective financing only for larger invoices or slow-paying clients

Success Factors

- Professional invoicing systems with clear terms and documentation

- Strong client relationships with creditworthy businesses

- Regular income patterns from repeat clients or ongoing projects

- Understanding of costs to ensure financing remains profitable

For freelancers meeting the basic criteria, invoice finance can provide valuable cash flow support, particularly when working with larger corporate clients who have extended payment cycles.

Next steps for invoice finance for agencies and consultancies funding project work on 30 90 day

Invoice finance for agencies and consultancies transforms the challenge of extended payment terms into an opportunity for improved cash flow and business growth. By converting unpaid invoices into immediate working capital, agencies can cover payroll, pay suppliers, and take on new projects without waiting 30-90 days for client payments.

The key to success lies in strategic usage rather than blanket financing. Focus on larger invoices from slower-paying clients while maintaining direct relationships with prompt payers. Choose between invoice factoring for hands-off collections or invoice discounting to preserve client confidentiality.

With funding available within 24 hours and costs typically lower than business overdrafts, invoice finance provides a flexible alternative to traditional lending. The absence of personal guarantees and focus on client creditworthiness makes it accessible for growing agencies regardless of their credit history.

Ready to improve your agency's cash flow? Check eligibility now with a 2-minute assessment that matches you with specialist invoice finance partners. No hard credit check required, and you'll receive fast decisions from providers who understand the unique needs of agencies and consultancies.

Further reading

Frequently asked questions

What Exactly Is Invoice Finance and How Does It Work for Creative Agencies?

Invoice finance transforms unpaid client invoices into immediate working capital by selling your outstanding receivables to a specialist finance provider. For creative agencies, this means getting paid within 24 hours instead of waiting 30-90 days for clients to settle their bills.

How Much Does Invoice Financing Cost Compared to Traditional Business Loans?

Invoice financing typically costs 1-5% of the invoice value, which often works out cheaper than business overdrafts or emergency funding when you factor in speed and flexibility. Unlike traditional loans with fixed monthly payments, you only pay fees on invoices you actually finance.

Can Small Design Consultancies Qualify for Invoice Factoring?

Small design consultancies can qualify for invoice factoring with monthly invoicing as low as £10,000, making it accessible for boutique agencies and growing consultancies. Approval focuses on client creditworthiness rather than consultancy size or trading history.

What Are the Risks of Using Invoice Financing for Marketing Agencies?

The main risks of invoice financing for marketing agencies include client relationship impacts, cost accumulation on slow-paying invoices, and potential disputes over work quality affecting payment. However, these risks are manageable with proper provider selection and clear client contracts.

Which Invoice Finance Providers Work Best for Digital Agencies Under 50 Employees?

Specialist invoice finance providers focusing on professional services and creative industries typically work best for digital agencies under 50 employees, offering flexible terms and understanding of project-based cash flow challenges.

How Quickly Can Agencies Get Cash Advances Against Outstanding Client Invoices?

Agencies can typically receive cash advances against outstanding invoices within 24 hours of approval, with some providers offering same-day funding for urgent cash flow needs. The speed depends on having pre-approved client lists and streamlined submission processes.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Reviewed by

UK business finance content reviewer

Robert reads our UK business finance guides before they go live, checking each one is accurate, easy to follow, and reflects how lending actually works today — not how a brochure says it should. He's listed on the FCA Register, approved as an SMF3 (AR) Executive Director at Switcha Limited, and connected to Lucky Growth Partners Ltd through its appointed representative relationship, so the regulated detail gets a properly qualified second read.

Sources

- plexcapital [2] Services - https://www.probfs.com/services/ [3] Invoice Factoring - https://www.voxfunding.com/solutions/invoice-factoring/ [4] blueroanef - https://blueroanef.com/ [5] Invoice Financing - https://www.crestmontcapital.com/invoice-financing [6] alternacs - https://alternacs.com/ [7] Accounts Receivable Financing - https://capitalax.com/accounts-receivable-financing [8] Invoice Finance - https://teybridgecapital.com/finance-option/invoice-finance/ [9] Construction Finance - https://www.fundsbygreenback.com/construction-finance

- British Business Bank finance options

- GOV.UK business finance support