Invoice Finance vs Business Loans: Which Funding Option Fits Your Business in 2026

Invoice finance lets you borrow against unpaid invoices and get cash within 24-48 hours, while business loans provide a lump sum with fixed monthly repayments over several years.

Quick answer

Invoice finance lets you borrow against unpaid invoices and get cash within 24-48 hours, while business loans provide a lump sum with fixed monthly repayments over several years. Invoice finance works best for B2B companies with reliable customers but poor cash flow timing, whereas business loans suit established businesses planning major investments or expansion.

Key takeaways

- Invoice finance approval depends on your customers' creditworthiness, not just your business credit score

- Funding speed differs dramatically: invoice finance delivers cash in 24-48 hours vs weeks for traditional bank loans

- Invoice finance fees range from 1.5% to 6% per invoice, while business loan rates typically run 6% to 13% APR

- Invoice finance scales with your sales volume, while business loans provide fixed lump sums

- B2B service companies with 30-90 day payment terms benefit most from invoice financing

- Business loans require comprehensive financial checks and often personal guarantees

- Invoice finance doesn't appear as debt on your balance sheet, preserving your credit profile

What Exactly Is Invoice Finance and How Does It Work

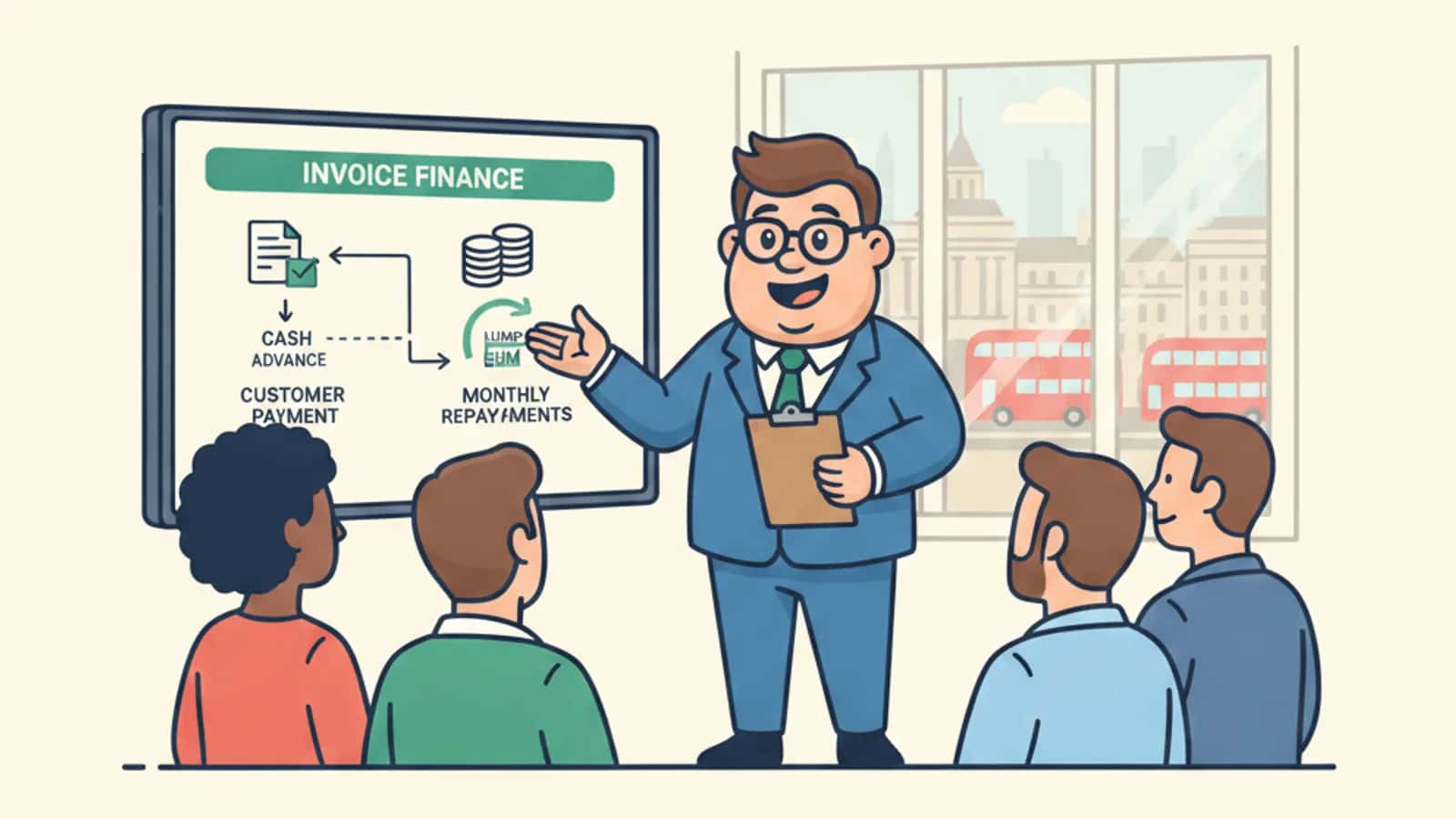

Invoice finance lets you borrow money against invoices you've already sent to customers but haven't been paid yet. You get cash immediately instead of waiting 30, 60, or 90 days for customer payments.

Here's the process: You submit unpaid invoices to a finance company. They advance you 70% to 90% of the invoice value within 24-48 hours. When your customer pays the invoice, the finance company takes their fee and sends you the remaining balance.

Two main types exist

- Invoice factoring: The finance company manages your sales ledger and collects payments directly from customers

- Invoice discounting: You keep control of customer relationships and collect payments yourself

The key difference from traditional business loans is that invoice finance uses your unpaid invoices as collateral, not your business assets or personal guarantees. The finance company primarily evaluates your customers' ability to pay, not your credit history.

Choose invoice finance if: You have reliable B2B customers but struggle with cash flow gaps between completing work and getting paid.

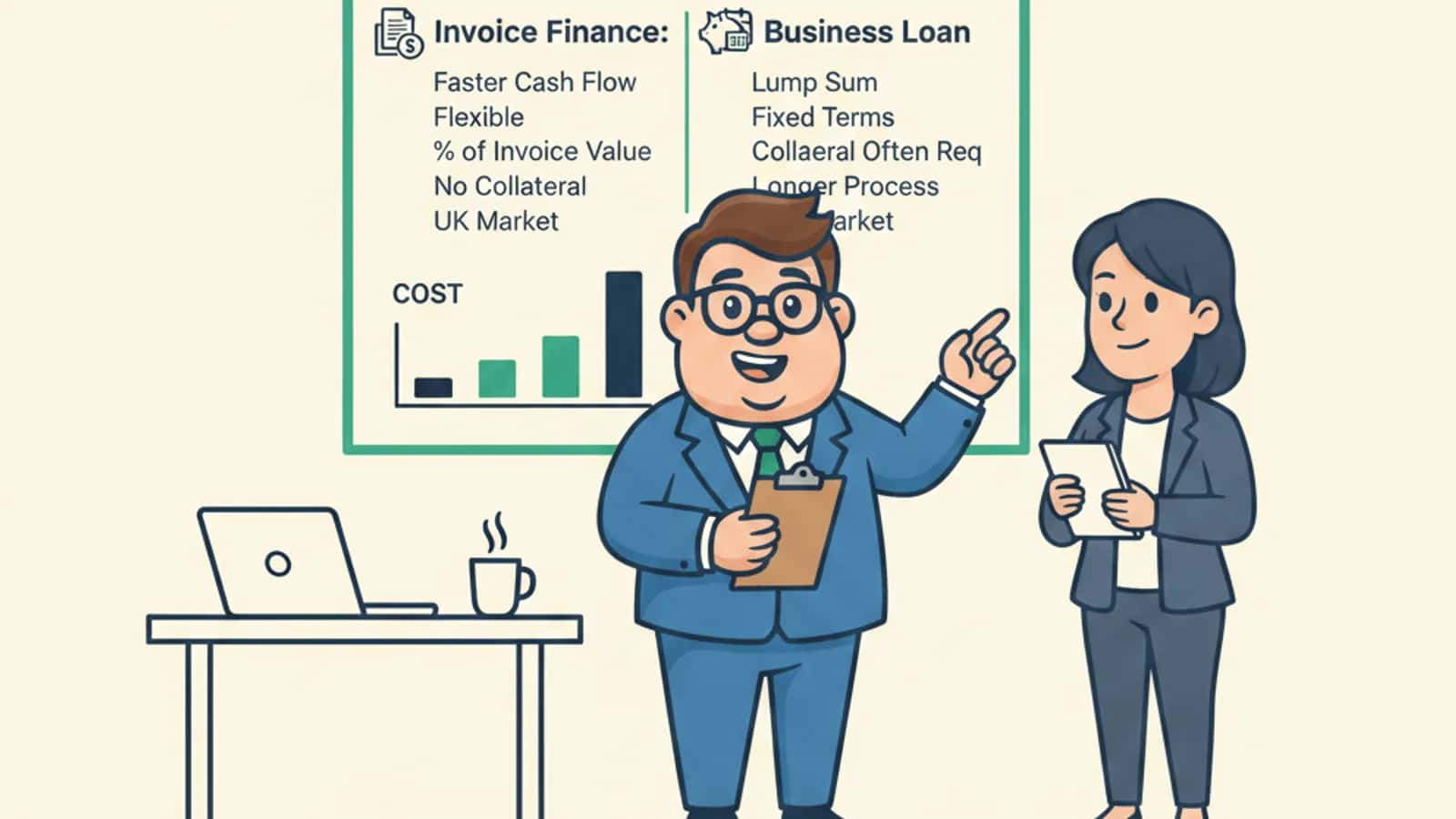

Which Option Is Cheaper: Invoice Finance vs Traditional Business Loans

Business loans typically cost less in pure interest terms, with rates averaging 6% to 13% APR. Invoice finance fees range from 1.5% to 6% per invoice, which can translate to 12% to 60% APR depending on how quickly customers pay.

Invoice finance costs include

- Discount fee: 1.5% to 6% of invoice value

- Service fee: 0.2% to 2% per month on outstanding invoices

- Setup fees: £200 to £1,000

Business loan costs include

- Interest rates: 6% to 13% APR for established businesses

- Arrangement fees: 1% to 3% of loan amount

- Early repayment charges: Varies by lender

However, cost comparison isn't straightforward. Invoice finance provides immediate cash flow relief when you need it most. Business loans require fixed monthly payments regardless of your cash position.

The cheaper option depends on timing: If customers pay invoices within 30 days, invoice finance costs stay reasonable. If payment terms stretch to 90 days, business loans become more cost-effective for long-term needs.

For businesses seeking flexible funding options, our unsecured business loans guide explains alternatives that don't require collateral.

How Much Can You Get: Invoice Financing vs Bank Loan Amounts

Invoice finance amounts depend on your monthly sales volume and invoice values. Most providers advance 70% to 90% of invoice value, with total facilities ranging from £10,000 to several million pounds.

Invoice finance limits

- Minimum: Usually £10,000 monthly invoicing

- Maximum: No fixed limit - scales with sales

- Advance rate: 70% to 90% of invoice value

- Customer concentration: Usually max 25% from single customer

Business loan amounts

- Unsecured loans: £10,000 to £500,000

- Secured loans: Up to £1 million or more

- Based on: Annual turnover, profitability, assets

- Fixed amount: Doesn't change with sales fluctuations

Invoice finance grows with your business automatically. Generate more invoices, access more cash. Business loans provide fixed amounts that may become inadequate as you grow or excessive during quiet periods.

Choose invoice finance for: Growing businesses with increasing sales volumes. Choose business loans for: Specific investment needs or equipment purchases.

Our cash flow business loans article covers options designed specifically for businesses with variable income patterns.

Pros and Cons of Invoice Finance for Small Businesses

Pros

- Fast access: Cash within 24-48 hours of invoice submission

- No fixed repayments: Only pay fees when you use the facility

- Scales with growth: More sales = more available funding

- Improves cash flow: Eliminates payment term gaps

- Credit-flexible: Approval based on customer creditworthiness

- Off-balance sheet: Doesn't appear as debt in accounts

Cons

- Customer dependency: Relies on clients paying invoices

- Higher costs: Can be expensive if customers pay slowly

- Limited to B2B: Requires invoiced sales to business customers

- Customer notification: Some types reveal financing to clients

- Concentration risk: Over-reliance on few large customers problematic

- Not suitable for all sectors: Retail and cash businesses excluded

Small businesses with seasonal sales patterns or long payment terms benefit most. Manufacturing companies, consultancies, and agencies often find invoice finance transforms their cash flow management.

When Should Startups Choose Invoice Finance Over Regular Business Loans

Startups should choose invoice finance when they have established B2B customers but limited trading history for traditional loans. New businesses often struggle with bank loan applications due to insufficient financial records, but invoice finance focuses on customer quality instead.

Which is right for you?

Invoice finance suits startups if

- Trading for 6+ months with regular invoicing

- B2B customers with good credit ratings

- 30-90 day payment terms causing cash flow gaps

- Limited assets for loan security

- Growing sales but poor credit history

Business loans suit startups if

- Need funds for equipment, premises, or stock

- Established trading history (12+ months)

- Strong personal credit scores

- Able to provide security or guarantees

- Predictable repayment capacity

Many startups combine both options. Use invoice finance for working capital and business loans for capital expenditure. This approach matches funding type to specific business needs.

For new businesses exploring their options, our business loan for startups guide covers eligibility requirements and application strategies.

Can You Qualify for Invoice Finance with Bad Credit

Yes, you can qualify for invoice finance with bad credit because approval primarily depends on your customers' creditworthiness, not your business credit score. Finance companies assess the likelihood of invoice payment, making your customers' financial strength more important than your credit history.

What matters for approval

- Customer credit ratings and payment history

- Invoice authenticity and validity

- Trading relationship duration with customers

- Industry sector and stability

- Monthly invoicing volume

What matters less

- Your personal credit score

- Business credit rating

- Previous loan defaults

- County Court Judgments (CCJs)

- Time in business (if customers are established)

However, very poor credit or recent insolvency may still cause problems. Some providers perform credit checks and may decline applications with serious adverse credit events in the past 12 months.

Choose invoice finance if: Your customers are creditworthy even if your business isn't. Avoid if: Your customers also have poor credit ratings or payment histories.

For businesses with credit challenges, our guide to business loans with no credit check explores options that focus on current trading performance rather than credit history.

What Types of Businesses Are Best Suited for Invoice Financing

B2B service businesses with payment terms of 30-90 days benefit most from invoice financing. The ideal profile includes regular invoicing, established customers, and cash flow gaps between completing work and receiving payment.

Best suited businesses

- Professional services: Consultancies, agencies, law firms

- Manufacturing: Companies with trade customers

- Construction: Contractors working with established builders

- Recruitment agencies: Temporary staffing providers

- IT services: Software development and support companies

- Transport and logistics: Freight and haulage operators

Less suitable businesses

- Retail: Cash sales don't generate invoices

- Restaurants: Immediate payment model

- Property: Long project cycles, complex payments

- Startups: Without established customer base

- High-risk sectors: Gambling, adult entertainment

Key requirements

- Minimum £10,000 monthly invoicing

- B2B customers (not consumers)

- Payment terms between 30-90 days

- Customers with good credit ratings

- No more than 25% concentration in single customer

Industry insight: Manufacturing and professional services account for approximately 60% of invoice finance users, reflecting their natural fit with the product structure.

Common Mistakes When Choosing Between Invoice Finance and Loans

The biggest mistake is choosing based on cost alone without considering cash flow timing and business model fit. Many businesses select the cheapest option upfront but struggle with repayment structures that don't match their income patterns.

Common mistakes:

- 1

Ignoring cash flow patterns

Choosing fixed loan repayments when income is seasonal or project-based

- 2

Focusing only on rates

Missing setup fees, early repayment charges, and hidden costs

- 3

Misunderstanding approval criteria

Applying for loans without adequate security or credit history

- 4

Wrong amount calculation

Borrowing too much or too little for actual needs

- 5

Not considering growth

Choosing fixed loans when scaling businesses need flexible funding

Decision framework

- Predictable income + specific purchase = Business loan

- Variable income + working capital needs = Invoice finance

- Growth phase + increasing sales = Invoice finance

- Established business + major investment = Business loan

For comprehensive guidance on loan applications, see our how to get a business loan guide covering preparation and approval strategies.

Speed Comparison: Invoice Finance vs Traditional Loan Funding Times

Invoice finance delivers funds within 24-48 hours of invoice submission, while traditional bank loans typically take 2-8 weeks for approval and funding. This speed difference often determines which option businesses choose during cash flow crises.

Invoice finance timeline:

- 1

Application

1-2 days

- 2

Approval

1-3 days

- 3

First advance

24-48 hours

- 4

Ongoing advances

Same day

Business loan timeline:

- 1

Application preparation

3-7 days

- 2

Bank review

1-2 weeks

- 3

Underwriting

1-3 weeks

- 4

Legal completion

3-7 days

- 5

Total

2-8 weeks

Factors affecting speed

- Invoice finance: Customer credit checks, invoice verification, simple documentation

- Business loans: Financial analysis, security valuations, legal documentation, committee approvals

The speed advantage makes invoice finance attractive for urgent working capital needs. However, this shouldn't drive hasty decisions about long-term funding strategies.

Choose invoice finance for: Immediate cash flow relief, seasonal peaks, unexpected opportunities. Choose business loans for: Planned investments, equipment purchases, expansion projects.

Our same day business funding article covers the fastest funding options available in 2026.

Risks of Using Invoice Finance for Cash Flow Management

The primary risk is customer dependency - your funding relies entirely on clients paying their invoices on time. If customers delay payments or dispute invoices, your cash flow problems worsen instead of improving.

Key risks

- Customer payment delays: Late payments increase costs and reduce cash flow

- Invoice disputes: Customers refusing to pay affects your funding

- Concentration risk: Over-reliance on few large customers

- Rising costs: Fees increase if customers consistently pay late

- Customer relationships: Some clients react negatively to finance company involvement

- Fraud risk: Incorrect or inflated invoices can trigger legal issues

Risk mitigation strategies

- Diversify customer base to avoid concentration

- Maintain strong customer relationships and communication

- Monitor customer credit ratings regularly

- Use invoice discounting to maintain customer control

- Keep accurate invoicing and delivery records

- Set clear payment terms and follow up promptly

When risks are highest: New customer relationships, seasonal businesses, sectors with payment disputes (construction), or businesses with poor invoice management systems.

Alternative approach: Some businesses use invoice finance selectively for their most reliable customers while maintaining traditional payment collection for others.

Service-Based vs Product-Based Businesses: Which Financing Fits

Service-based businesses typically suit invoice finance better because they generate regular invoices with clear payment terms, while product-based businesses often benefit more from business loans for inventory and equipment financing.

Service businesses and invoice finance:

Service companies create invoices after completing work, generating immediate funding opportunities. Professional services, agencies, and consultancies typically have 30-60 day payment terms, making invoice finance a natural fit.

Advantages for services

- No inventory to finance upfront

- Clear invoice values and payment terms

- Established customer relationships

- Predictable payment patterns

Product businesses and business loans:

Manufacturing and retail businesses need funding for stock, equipment, and premises before generating sales. Business loans provide upfront capital for these investments.

Advantages for products

- Fund inventory purchases

- Equipment and machinery financing

- Premises and expansion costs

- Fixed costs independent of sales timing

Hybrid approach: Many product businesses use both options - business loans for capital expenditure and invoice finance for working capital once they establish trade customers.

Exception: Product businesses selling to other businesses on credit terms can benefit from invoice finance for their trade sales, even while using loans for inventory.

What Happens If Customers Don't Pay Their Invoices

When customers don't pay invoices, the outcome depends on whether you chose invoice factoring (with recourse) or non-recourse factoring, and the specific terms of your agreement with the finance provider.

With recourse agreements (most common):

You remain responsible for unpaid invoices. If customers don't pay within agreed timeframes (usually 90-120 days), you must buy back the debt from the finance company. This protects the lender but leaves you with the original problem plus financing costs.

Non-recourse agreements (less common):

The finance company accepts the risk of customer non-payment. They cannot claim money back from you if customers default. However, this protection costs more and often excludes disputes about goods or services quality.

Typical process for unpaid invoices:

- 1

Days 1-30

Normal collection procedures

- 2

Days 31-60

Escalated collection efforts

- 3

Days 61-90

Final demands and formal notices

- 4

Days 90+

Debt buy-back required (recourse) or write-off (non-recourse)

Protection strategies

- Credit insurance on major customers

- Diversified customer base

- Clear terms and conditions

- Regular customer credit monitoring

- Strong invoice and delivery documentation

Next steps for invoice finance vs business loans

The choice between invoice finance vs business loans depends on your business model, cash flow patterns, and funding needs. Invoice finance works best for B2B service companies with reliable customers but poor payment timing, while business loans suit established businesses making specific investments or purchases.

Invoice finance offers speed and flexibility but costs more and depends entirely on customer payments. Business loans provide cheaper, predictable funding but require stronger credit profiles and longer approval processes.

Which is right for you?

Choose invoice finance if you

- Have regular B2B invoicing over £10,000 monthly

- Face cash flow gaps due to 30-90 day payment terms

- Need flexible funding that scales with sales

- Have creditworthy customers but limited business credit history

Choose business loans if you

- Need funds for equipment, premises, or major investments

- Have predictable income and can manage fixed repayments

- Want the lowest cost funding option

- Have strong credit history and can provide security

Many successful businesses use both options strategically - invoice finance for working capital and business loans for growth investments. The key is matching funding type to specific business needs rather than choosing based on cost alone.

Ready to explore your options? Check Eligibility Now with our 2-minute assessment. No hard check to start, and you'll see matched funding options from our wide partner panel. Business funding without the fuss.

Further reading

Frequently asked questions

What Exactly Is Invoice Finance and How Does It Work?

Invoice finance lets you borrow money against invoices you've already sent to customers but haven't been paid yet. You get cash immediately instead of waiting 30, 60, or 90 days for customer payments.

Which Option Is Cheaper: Invoice Finance vs Traditional Business Loans?

Business loans typically cost less in pure interest terms, with rates averaging 6% to 13% APR. Invoice finance fees range from 1.5% to 6% per invoice, which can translate to 12% to 60% APR depending on how quickly customers pay.

How Much Can You Get: Invoice Financing vs Bank Loan Amounts?

Invoice finance amounts depend on your monthly sales volume and invoice values. Most providers advance 70% to 90% of invoice value, with total facilities ranging from £10,000 to several million pounds.

When Should Startups Choose Invoice Finance Over Regular Business Loans?

Startups should choose invoice finance when they have established B2B customers but limited trading history for traditional loans. New businesses often struggle with bank loan applications due to insufficient financial records, but invoice finance focuses on customer quality instead.

Can You Qualify for Invoice Finance with Bad Credit?

Yes, you can qualify for invoice finance with bad credit because approval primarily depends on your customers' creditworthiness, not your business credit score. Finance companies assess the likelihood of invoice payment, making your customers' financial strength more important than your credit history.

What Types of Businesses Are Best Suited for Invoice Financing?

B2B service businesses with payment terms of 30-90 days benefit most from invoice financing. The ideal profile includes regular invoicing, established customers, and cash flow gaps between completing work and receiving payment.

Written by

The Funding Fred Editorial Team creates plain-English guides to help business owners understand funding options, eligibility, and application readiness before they compare finance options.

Reviewed by

UK business finance content reviewer

Robert reads our UK business finance guides before they go live, checking each one is accurate, easy to follow, and reflects how lending actually works today — not how a brochure says it should. He's listed on the FCA Register, approved as an SMF3 (AR) Executive Director at Switcha Limited, and connected to Lucky Growth Partners Ltd through its appointed representative relationship, so the regulated detail gets a properly qualified second read.